The second quarter began against a backdrop of continued geopolitical uncertainty in the Middle East, with markets still assessing the implications of the conflict between Iran and the US. As the period progressed, however, those concerns eased as the two nations agreed to continue peace talks, helping to reduce fears of a more prolonged escalation.

The easing in geopolitical tensions was most clearly reflected in oil markets. Crude prices fell back over the quarter, taking some pressure off inflation expectations and providing a more supportive backdrop for risk assets. This shift also helped move investor attention away from energy and inflation, and back towards the dominant market theme of artificial intelligence.

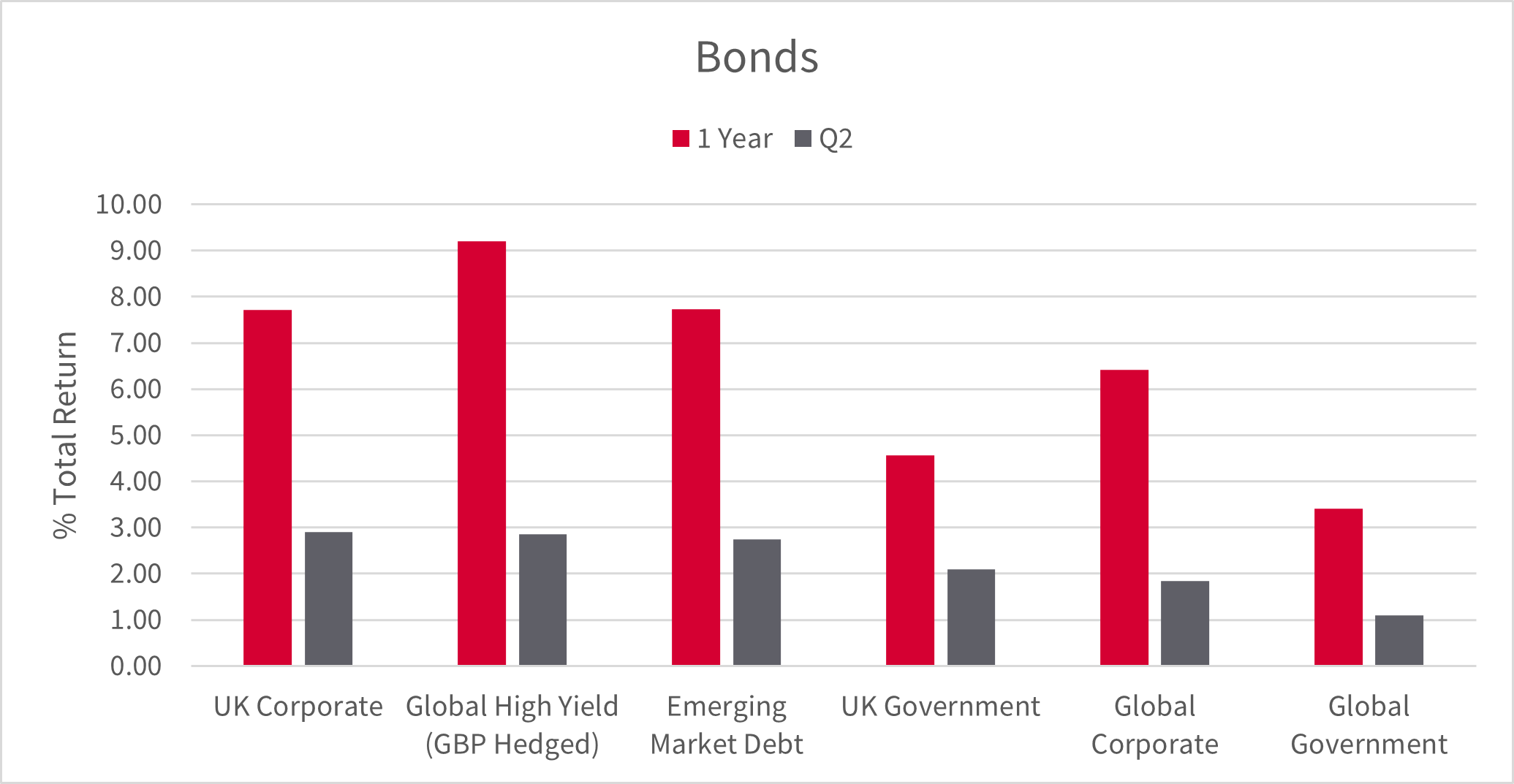

Bond markets remained volatile for much of the quarter, with government bond yields staying elevated as investors continued to weigh the path of inflation, central bank policy and fiscal risk. Central banks were an important driver of that volatility. In Europe, policymakers responded to the inflationary impulse from higher energy prices by raising rates, while in the UK the expected path for interest rates moderated considerably as oil prices fell back and growth concerns became more prominent.

The US saw a notable shift in Federal Reserve leadership, with Jay Powell giving way to Kevin Warsh. Markets interpreted the change as the start of a potentially different communication regime, with Warsh placing less emphasis on forward guidance. While the Fed left rates unchanged, the leadership transition and the possibility of a less predictable policy framework contributed to uncertainty in rates markets. Towards the end of the period, however, bond markets rallied as yields moved lower into quarter end, providing some relief after a volatile start to the year.

Source: AJ Bell and Morningstar, As of 30/06/26. Total returns represent those in GBP terms.

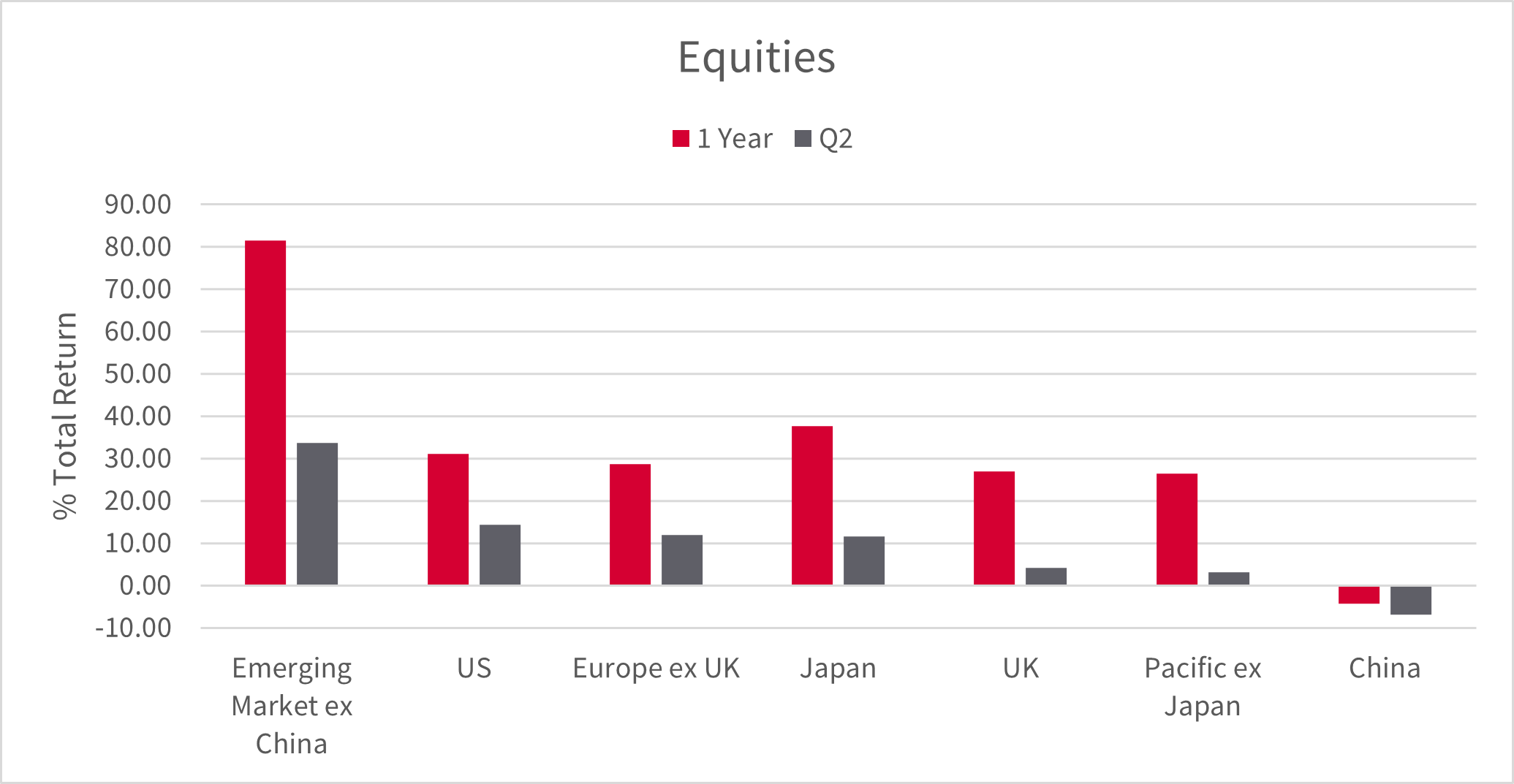

Equity markets were increasingly led by the artificial intelligence theme as the quarter progressed. Emerging markets ex China delivered particularly strong returns, with South Korea a standout performer as investors continued to reward companies exposed to the AI memory and semiconductor supply chain.

In the US, the AI theme also remained highly influential, with renewed investor enthusiasm reinforced by market attention around major technology-related listings and the continued build-out of AI infrastructure. Returns were more muted in areas less directly exposed to this theme. China remained weaker as the domestic economy continued to face pressure, while the UK also lagged, with the earlier support from energy exposure fading as oil prices declined.

Source: AJ Bell and Morningstar, As of 30/06/26. Total returns represent those in GBP terms.

Looking ahead, the AI theme has returned to the centre of investor attention as geopolitical risk has faded somewhat into the background. Political risk appears somewhat heightened in the UK following the Prime Minister’s resignation, but further afield investors are more focused on how best to gain exposure to the dominant AI trend and how much of that opportunity is already reflected in valuations.

For portfolios, returns were generally stronger than in the first quarter, helped by a more settled market backdrop as volatility subsided somewhat. While conditions remained far from straightforward, the easing in geopolitical concerns, lower oil prices and improved sentiment towards risk assets provided a more supportive environment for diversified portfolios.

The key challenge now is balancing exposure to the powerful AI theme with appropriate risk control. Diversification remains essential, but the quarter has reinforced that it needs to be considered not just at a geographic level, but also across sectors and sources of return.

As we move into the second half of 2026, maintaining a balanced approach across asset classes, regions and sectors appears increasingly important. The opportunity set remains attractive, but with market leadership narrow and investor enthusiasm concentrated in a small number of themes, portfolio resilience and disciplined diversification are likely to remain central to delivering good client outcomes.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.