As summer arrived, markets started to become more relaxed about the trade war and political theatre in Washington. Instead, investors turned their attention back to fundamentals and the dominant AI theme. There was little change in the economic backdrop with respect to growth across most regions, however, greater concern arose in the US after a significant downward revision to payroll data and weakness through the summer months. Whilst the US dollar is weaker in 2025, it stabilised versus major peers during the quarter and made some ground back versus the pound.

The risks to inflation that we have been flagging for some time started to emerge in earnest in the UK, with inflation now expected to reach double the Bank of England target before year end. In the US, inflation pressures also arose, although there were signs that companies absorbed some price pressures through margins rather than passing them on to consumers amidst economic uncertainty.

Bond markets started to price in greater inflation uncertainty, with longer-dated bond yields moving higher throughout the quarter in many markets. Fiscal uncertainty also loomed over the UK and US bond markets, however, in the US this was counteracted by the Fed quickly responding to weaker employment statistics via a “risk management” rate cut in September. At a time of political pressure on the central bank, significant dispersion arose amongst the Fed’s voting members, with one suggesting interest rates should fall to below 3% by year end

Back in the UK, inflation pressures similarly complicated the Bank of England’s path. Sticky price increases in core goods, housing, and services make calibration difficult. The UK yield curve steepened slightly as markets struggled to pin down the inflation and growth trade-off. Corporate bonds performed resiliently as credit spreads compressed again, delivering good returns across investment grade and high yield markets.

Source: AJ Bell and Morningstar, as of 30/09/25. Total returns represent those in GBP terms.

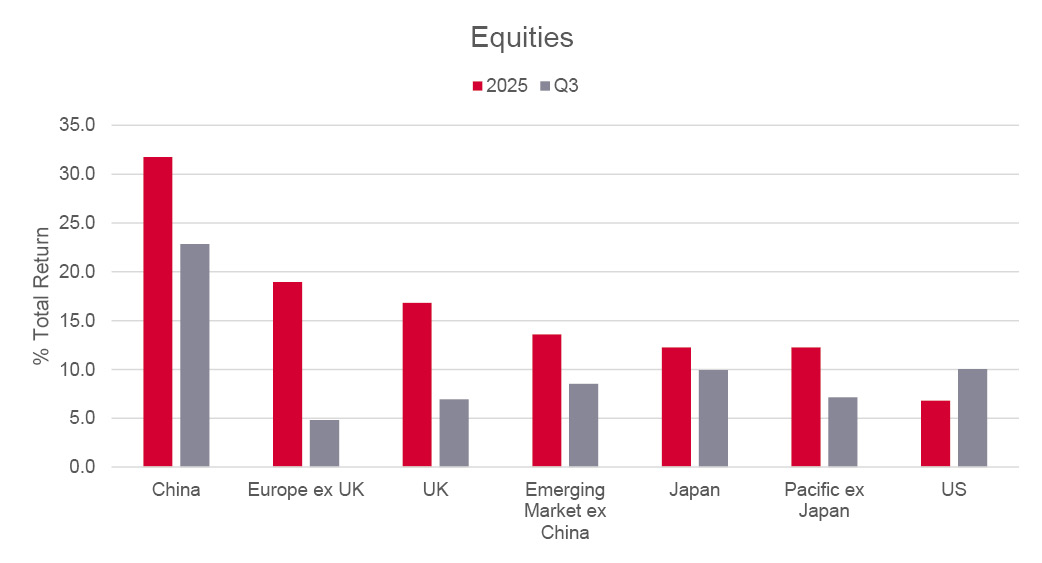

The leadership rotation in global equities gained traction again this quarter. While the US market continued to deliver gains and be powered by the AI theme, its returns stood amongst some other good performances. China stole the show as AI technology continued to emerge and attract investors to the offshore market, where tech sector valuations are much lower than those seen in the US. Broader emerging markets also performed well. Strong returns from TSMC in Taiwan and a continued rally in Korea were however weighed down by weakness in Indian equities.

Europe and the UK also advanced, particularly large caps in the UK. However, returns fell short of other regions. In Japan, the equity market picked up after a hard-fought trade deal with the US and the reassertion of good company fundamentals, not least that they continue to undertake large-scale buybacks.

Source: AJ Bell and Morningstar, as of 30/09/25. Total returns represent those in GBP terms.

The improving mood through the summer brings year- to-date returns in many equity markets into double-digit territory. However, the weaker dollar over the course of the year has eroded returns for UK investors significantly.

The contrast between the equity and bond markets is becoming interesting, particularly in the US where bond yields are increasingly displaying fears over the economic growth trajectory, whilst equities remain squarely focused on AI, the associated capex and signs of strong sentiment in M&A activity. Bond markets are often early to point out cracks in the economy that may worry equities later, however they can also cry wolf. Meanwhile, gilt investors in the UK have other issues to worry about, namely inflation and how it can be tamed without causing economic damage. Plenty of headlines regarding these problems stand between us and the end of the year, however, as we often see, they may just prove to be noise best avoided by those managing portfolios.

The value of investments can go down as well as up and your client may not get back their original investment.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.