Advisers have an important message for clients: use the full ISA allowance as soon as possible as it could pay off in more ways than one.

The new tax year is upon us, which means putting an investment plan into action. Putting it off until another day is a lost opportunity to make money. It’s not just about being organised with life admin, it’s also about giving an ISA more time to work its magic.

Research by AJ Bell found that someone who had put £5,000 into an ISA at the start of every tax year since 1999, and invested in a typical global equity fund, would now be £25,000 better off than someone who didn’t invest until the last day of the tax year.

Making the most of an ISA also brings tax advantages compared to leaving money in a general investment account, which is particularly important now that dividend tax rates have gone up. Putting money into ISA locks in generous tax benefits, so the investor pays nothing to the taxman on future capital gains or income for investments inside the wrapper.

Those who invest outside tax wrappers must now contend with raised dividend tax rates – up by two percentage points to 10.75% for basic rate taxpayers, and to 35.75% for higher rate taxpayers. The additional rate is unchanged at 39.35%. The changes came into effect on 6 April 2026.

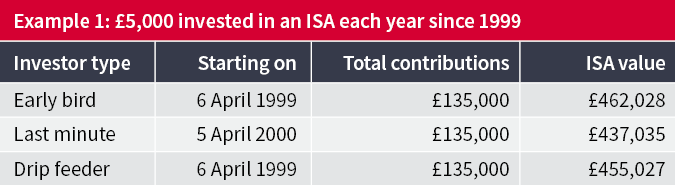

We ran scenarios that compared investing in a typical global fund every year since ISAs began in 1999.

Early-bird Erin put £5,000 into her ISA on the first day of each tax year (6 April) and invested in a typical global fund. Up until the end of the most recent tax year (5 April 2026), she would have paid in £135,000 and is now sitting on a pot worth £462,028.

Last-minute Linda also put £5,000 a year into her ISA , but left it until the last day of each tax year (5 April). The difference in returns is striking. Even though both Erin and Linda contributed the same £135,000 to their ISAs, Linda’s pot is only worth £437,035 – an astonishing £24,993 less than Erin’s ISA.

Early-birds benefit from having extra time in the market. Markets go up and down, but they generally rise more than they fall. Since 1999, the typical global fund has returned on average 8% from the beginning to the end of each tax year and has made a positive return in 17 out of 27 tax years. So around two-thirds of the time you would have been better off investing at the start of the tax year, rather than waiting until the end.

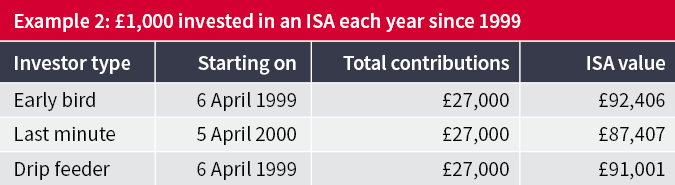

Source: AJ Bell, FE Analytics, total return of IA Global sector average in GBP to 5 April 2026. Early bird ISA investor invests on the 6 April each tax year; last minute ISA investor invests on the 5 April each tax year; drip feed ISA investor invests on the 6th of each month

Source: AJ Bell, FE Analytics, total return of IA Global sector average in GBP to 5 April 2026. Early bird ISA investor invests on the 6 April each tax year; last minute ISA investor invests on the 5 April each tax year; drip feed ISA investor invests on the 6th of each month

So, how would the numbers stack up if money was drip fed into an ISA rather than as an annual lump sum? Drip-feed Diana paid £416.67 into her ISA every month, beginning on 6 April 1999. In a single year that contribution adds up the same £5,000 as Erin’s and Linda’s lump sum payments. By 5 April 2026, Diana’s ISA was worth £455,027 which is better than Linda’s ISA but not quite as good as Erin’s.

While the early-bird investor gets a head start over others, drip feeding money into an ISA can still be a rewarding strategy as it doesn’t involve trying to time the market. Over a long period, money is fed into the account in both good and bad conditions. When markets are high, the money buys fewer shares or fund units – but when markets are low, you get more bang for your buck. It’s also hassle-free and takes the emotion out of investing.

As an aside, those who deployed their new £20,000 ISA allowance at the start of the latest tax year would have positioned themselves to ride the recovery in global markets that happened a moment later. The first trading session of the new tax year was Tuesday 7 April and markets rallied hard on the following day. Those who hadn’t invested their new allowance on 7 April would have missed the bulk of the gains that happened at the market open on 8 April.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.