Frozen tax thresholds punish taxpayers by stealth. When asset prices rise but thresholds fail to track inflation, the result is higher tax bills.

Astonishingly, the main inheritance tax (IHT)-free threshold won’t have changed in over two decades by the time the freeze is lifted in 2030.

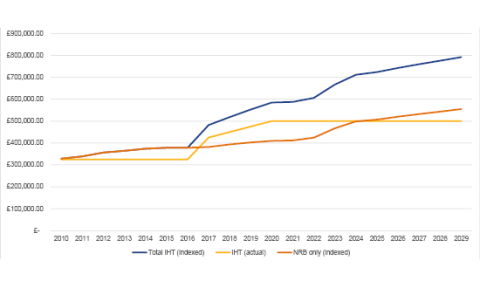

Although a new exemption has been introduced since then – the residence nil rate band (RNRB) – the figures below show it doesn’t actually compensate for frozen thresholds. Had government done nothing whatsoever other than index the IHT allowance to CPI over the last 20 years then the tax-free limit would be almost £1.1 million for a married couple in 2030.

Clients with an estate over this sum stand to pay an extra £44,000 in death duties as a result.

Had both the nil rate band and the more recently introduced RNRB both been index linked by default then the total IHT-exempt threshold would be over £1.58 million. Were that the case it would shave £234,000 off IHT bills for some families.

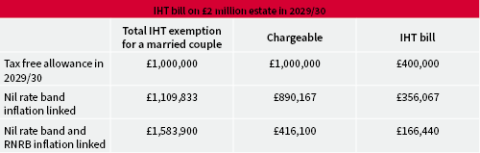

The tax bill on a £2 million estate will be £400,000 thanks to frozen thresholds. That would be reduced to £166,000 if the exemption for the combined assets of a married couple had been uprated.

IHT bill on £2 million estate in 2029/30:

Source: AJ Bell. Nil rate band indexed in April based on previous September’s CPI. Residence nil rate band indexed from 2021. Future years use OBR forecast annual inflation. Married couple IHT on last death in 29/30.

For larger estates over £2 million the story is even worse, since the RNRB is gradually tapered away for households with cash and assets to pass on above this level. This is likely to be exacerbated by the inclusion of unspent pensions within taxpayer’s estates from April 2027.

How the IHT threshold would have looked without the two-decade freeze:

Source: AJ Bell. Nil rate band indexed in April based on previous September’s CPI. Residence nil rate band indexed from 2021. Future years use OBR forecast annual inflation. Based on a single person.

The government likes to tell us only 1 in 20 estates currently pays IHT, but their own figures show the amount they are raking in was already going up before the changes announced in the Budget.

New rules (that are being consulted upon) for unspent pensions to get dragged into the IHT net from 2027 could result in higher bills for nearly 50,000 estates. That’s before the impact of the extra two-year freeze in thresholds will be felt, which HMRC estimates will impact another 4,300 new estates.

So, what can you do now if you think your client’s estate might be affected? Here are three ways in which they can reduce the impact of IHT on their loved ones:

If your clients die without a will, their estate will fall under the intestacy rules. This could mean a higher IHT bill and if they have no surviving relatives, the rules can even pass their wealth to the Crown. Unmarried partners do not have the same rights as those in a marriage or civil partnership – even when they have lived together for many years – and under the intestacy rules, they will not inherit. If your client already has a will, it’s a good idea to remind them to review it and keep it up to date. They can use their will to detail their funeral wishes, and most funeral expenses are generally deductible for IHT.

If they have significant assets, estate planning using trusts can also help mitigate a tax bill. Trusts and taxation are complex areas, so they should seek professional advice from both you and a solicitor to avoid any costly mistakes.

There are gifts your client can give each tax year that are exempt from IHT and reduce the value of their estate. The ‘annual exemption’ allows your clients to give away a total of £3,000 each year, either to one person or split between several. Your clients can also bring forward unused annual exemption for one year. Unlimited ‘small’ gifts of up to £250 per person can be made, if they haven’t already used their annual exemption on the same person.

Tax-free gifts to someone getting married or entering a civil partnership are also available: up to £5,000 for a child, £2,500 to a grandchild or great-grandchild, or £1,000 to anyone else. These can be combined with other allowances but to meet the rules, a wedding gift must be made before the wedding itself, and the wedding must go ahead.

Other gifts that are not exempt or within the allowances above are called potentially exempt transfers, meaning they only escape IHT if your clients survive for seven years after making them. If your clients die within seven years then the value of the gift is added back into their estate, but taper relief might reduce the rate of IHT on it if at least three whole years have passed. A powerful gifting allowance that is often missed is making gifts from excess income. Your clients can set up regular gifts from their extra income without limit – for example to help towards grandchildren’s school fees or invest in their Junior ISA – provided you can show that they do not reduce your client’s standard of living. The best way to evidence this is to keep records of your client’s regular income and show that they’re not having to cut back on their normal spending to make them. The records will also be needed when it comes to administering your client’s estate and claiming the exemption.

Depending on cost, your clients could find life insurance is a simple way to fund a likely IHT bill, or to cover large gifts made in the past seven years. Your clients should also review any life insurance they already have, particularly anything they’ve got through their employer. That’s because the payouts from policies can count as part of the estate unless your client’s policy is written in trust.

Writing policies in trust removes them from their estate and means your client’s loved ones don’t have to wait for probate to make a claim. As IHT must normally be paid within six months to avoid interest and needs to be settled before probate is granted, insurance could make things easier for your client’s loved ones and prevent assets having to be sold to help pay any bill.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.