Central banks are increasingly turning their attention to any economic softness that is being caused by higher interest rates, having spent much of the last three years focused on the high levels of inflation. The starting gun has now finally been fired on the rate cutting cycle. The Bank of England (BoE) and European Central Bank (ECB) have led the field in terms of the major central banks, and in the US the Federal Reserve (Fed) is widely anticipated to cut by 25 basis points (bps) or 50bps at its meeting finishing on 18 September. With returns on cash-like investments such as Money Market Funds (MMFs) reflecting these rate cuts almost instantaneously, what are the prospects for cash returns going forward?

Firstly, some context. MMFs became increasingly popular throughout 2023 as rates on cash-like investments rose to levels not seen since the Global Financial Crisis and market expectations of the first rate cuts fell woefully short. Many DFMs, including AJ Bell Investments, launched associated MPS products to provide a solution that enabled advisers to reduce the friction associated with moving assets on and off platforms. It also gave access to cash-like investments that customers may have not considered previously for their on-platform investments. Here at AJ Bell, we took the innovation a step further and offered the Money Market MPS with no associated Annual Management Charge (AMC).

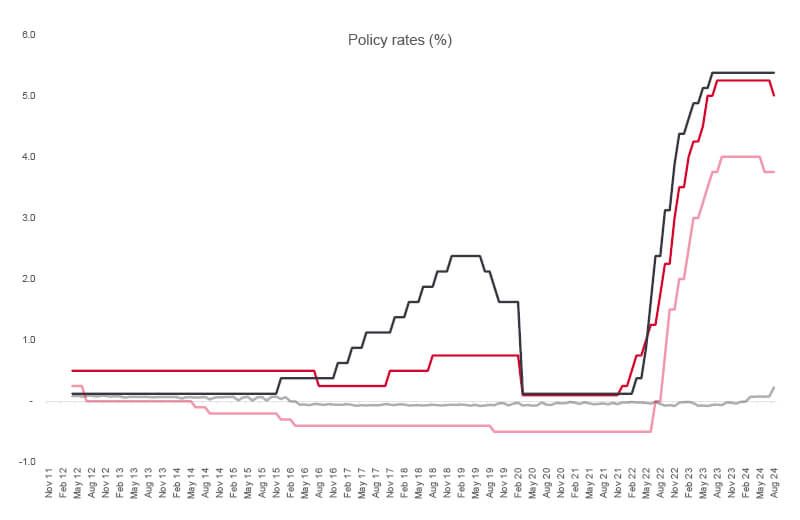

There have been several false starts for interest rate expectations versus reality in the last two years. We shall focus on the Fed for now, as they, in many respects, remain the world’s central bankers (despite some of the recent naysayers, US dollars make their way into almost every aspect of global capital markets). In early 2023 it was anticipated that the Fed would cut by summer 2023, which then became autumn … and then winter. The second half of 2023 witnessed some extraordinary jostling in rate expectations, moving from seemingly none on the horizon to suddenly eight throughout 2024! That was walked back again through the early part of 2024 and lands us more or less to where we are now.

2024 has indeed seen several central banks cutting interest rates, the ECB and the BoE being the most notable initial movers. There is a certain irony in the move from the BoE. In the UK, there was a painful period of economic performance and even a very mild recession in the second half of 2023. In early 2024 the economic data began to improve and continues to look relatively rosy. After a delay in July because of the election, necessitated by the need to be seen as staying out of the political debate, the BoE made a cut in August. 25bps to 5% gets them off the mark in a race to what the market suggests is 3.75% by August 2025.

Source: Bank of England, Federal Reserve, European Central Bank & Bank of Japan.

The BoE, like everyone else, is looking over their shoulder at the Fed. The Fed will lead the rest at some point, physically or perhaps only metaphorically providing an element of confirmation bias to other central bankers and cheering them on.

For investors holding cash or cash-like investments there is a perception that risk is low, however that depends entirely on which risks you are looking to define. From a volatility and drawdown perspective yes, these are lower risk investments, however they do have to navigate a hurdle or two: reinvestment risk and inflation. Now that inflation has fallen back to more benign levels, the focus is on reinvestment risk, which presents itself upon maturity of the investment if the cash flow cannot be reinvested at the equivalent rate of return available at outset, leaving a reduced prospective income and total return to be derived from the investment. For cash investors this risk arises quickly as interest rates go down. The rate they receive on cash or MMFs falls as those investments mature and can only be reinvested at the new lower interest rate.

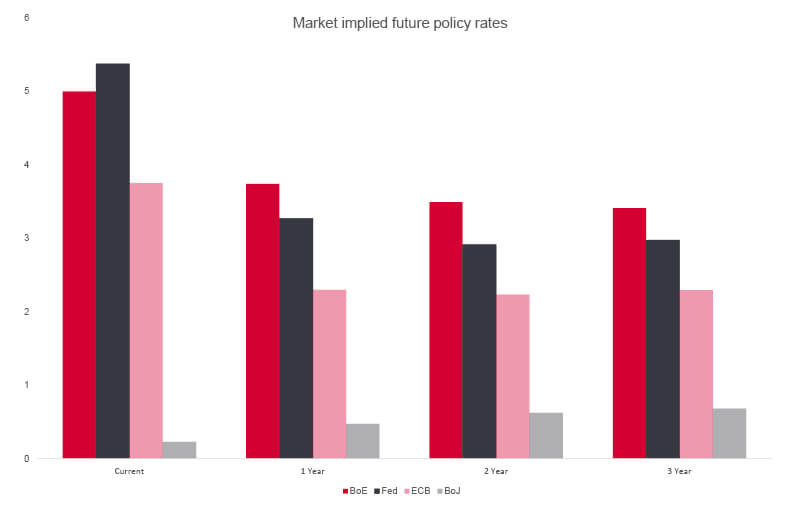

The question will increasingly become: is this a marathon or a sprint? Typically, it is a sprint – interest rates are said to ‘go up the escalator and down the lift shaft’. This is either in response to some unforeseen event or the revelation of the true damage higher interest rates have been inflicting on the economy. The key for investors here is consensus. As you can see in the chart below, of the interest rate expectations over the next three years, the market is already pricing in several cuts. The Bank of Japan (BoJ) is an outlier, but we will not add to the column inches being generated by Japan here.

Source: AJ Bell, as of 05/09/2024.

If rates were cut more aggressively than the current market expectations, i.e. below the 3.4% trough shown for UK rates, there could be value yet to be extracted from bond markets by moving out of cash and further out the yield curve, for example, by locking in current rates on shorter maturity gilts. This however depends on why you hold cash in the first place. Those seeking the relatively low volatility and drawdown potential of cash are probably not looking to take on the incremental volatility of bonds. For those that have been attracted to the yield of cash, gilts may still be worth a look, although some of the opportunity has been missed as yields have compressed over the summer.

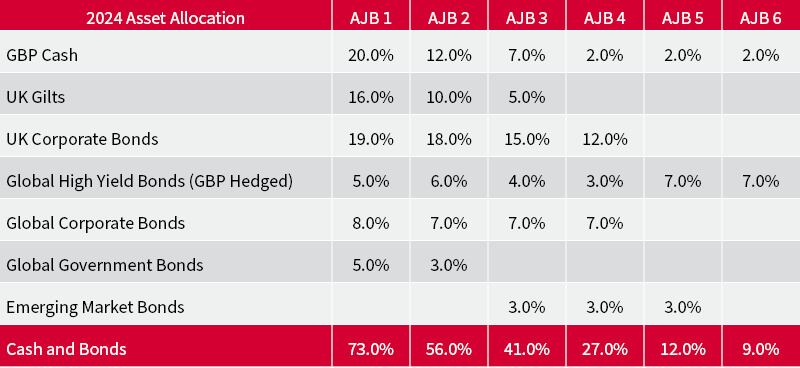

To navigate reinvestment risk within the AJ Bell Funds and MPS we set the 2024 asset allocations with what we deemed to be a ‘neutral’ level of interest rate risk (fixed income duration in the region of five to six years). In other words, we would receive capital compensation on our bond holdings to help offset the reinvestment risk posed by that of cash, but crucially are not taking too much risk should inflation reassert itself and rates stay ‘higher for longer’. The allocation to GBP cash and equivalents has generally been a positive so far this year, but as we emerge from summer the duration we have taken in gilts and US Treasuries has been increasingly important.

The value of investments can go down as well as up and your client may not get back their original investment.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.