Traditional portfolio asset allocation tends to start with equities and bonds, with a bit of a cash buffer thrown in, before thoughts move to areas that are designed to provide some diversification, in the theory (or hope) that their performance does not correlate with (or mirror) that of the other options. These ‘alternative’ areas can include commodities, commercial property or even private equity funds, but one area which may still be flying a little under the radar is infrastructure.

“Infrastructure as an asset class has performed well for a decade or more.”

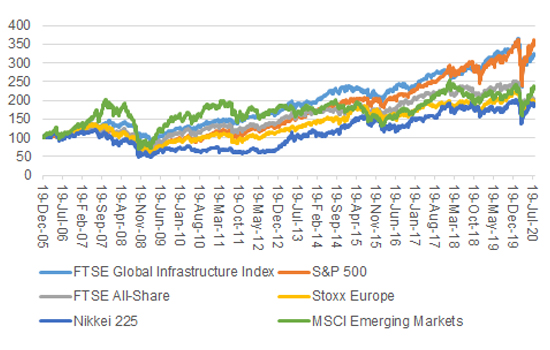

This is surprising in some ways, since infrastructure as an asset class has performed well for a decade or more. Looking at it from the perspective of only listed firms in this field, infrastructure stocks have outperformed all of the major geographic indices bar the super, soar-away USA, which continues to benefit from the barnstorming run generated by Facebook, Alphabet, Amazon, Apple, Netflix and Microsoft.

Listed infrastructure plays have performed well in a global equity context

Source: Refinitiv data

While we must all accept that past performance is no guarantee for the future, the past 15 years’ data may give advisers and clients some confidence that infrastructure is at least no flash in the pan. In addition, the asset class has several other facets which mean it may be worthy of consideration as a part of a balanced, diversified portfolio, especially for those investors who have a long-term time horizon and are seeking income.

“Beyond the tempting past performance record, there are four other reasons why infrastructure may suit the overall strategy, target returns, time horizon and appetite for risk of certain advisers and clients.”

A selection of companies, held directly or via a fund, which own or operate assets ranging from ports to airports, toll roads to pipelines and essential water and electricity utilities may not appeal to everyone – the thought of owning a stake in an airport in particular right now could leave many investors feeling green at the gills. But, beyond the tempting past performance record – which appears to show strong total returns over the past 15 years and with lower volatility than most equity benchmarks – there are four other reasons why infrastructure may suit the overall strategy, target returns, time horizon and appetite for risk of certain investors.

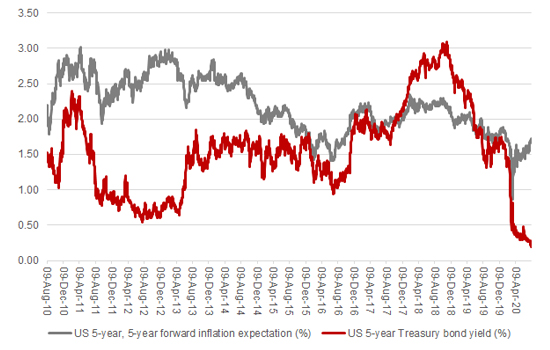

“Some advisers and clients may not be convinced by talk of inflation but the US five-year forward inflation expectation indicator is ticking higher.”

Inflation expectations are slowly creeping higher

Source: Refinitiv data, FRED – St. Louis Federal Reserve database

Inflation expectations are slowly creeping higher

Source: Refinitiv data, Association of Investment Companies for the Infrastructure and Renewable Energy Infrastructure categories

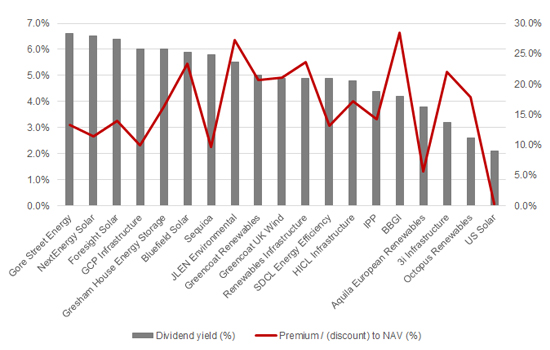

“There is no free lunch. Infrastructure stocks (and the collectives which own them) need to offer a yield to compensate advisers and clients for the risks involved, which can include regulation, political interference and top-line growth that is usually modest at best.”

As ever, however, there is no free lunch. Infrastructure stocks (and the collectives which own them) need to offer a yield to compensate advisers and clients for the risks involved, which can include regulation, political interference and top-line growth that is usually modest at best. In addition, the UK-listed investment trusts come with an annual fee and they also currently trade at lofty premiums to their net asset value. At least some of their potential is therefore factored into valuations already and, by paying that premium, investors are effectively giving away some of their future returns. Patience will therefore be required if anyone does feel infrastructure is a suitable option for them, once they have done their own research.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.