An aggregation of analysts’ forecast for all of the FTSE 100’s members suggests that the index offers a dividend yield of 3.6% for 2020 and 4.4% for 2021. Those figures may look alluring to income-hunters, especially as the Bank of England base rate looks pretty firmly anchored at 0.1% – and the next move there could even be down, into negative territory, if some of the most recent rhetoric from Governor Andrew Bailey is taken at face value.

However, we began the year with the same analysts’ forecasts putting the FTSE 100 on a yield of 4.8% for 2020. Since then, dividend forecasts have been cut by a third and the index has fallen by a sixth, to add the insult of capital losses to the injury caused by lost income.

“We began the year with the same analysts’ forecasts putting the FTSE 100 on a yield of 4.8% for 2020. Since then, dividend forecasts have been cut by a third and the index has fallen by a sixth.”

Before they make any investment case for the UK on the basis of its yield, therefore, advisers and clients must look at the forecast source of the dividends and whether the forecasts are reliable.

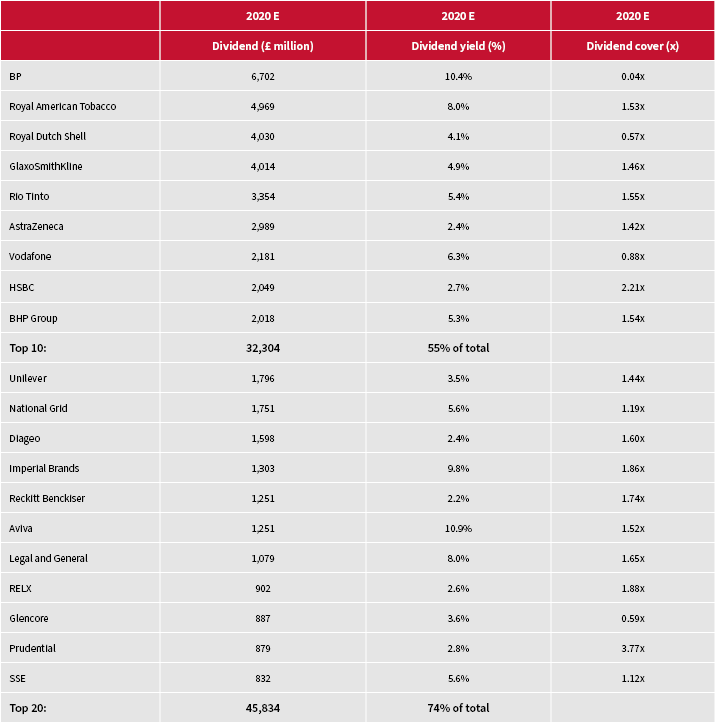

The first thing to note for anyone buying UK equities for their income, either through an actively-managed or a passive fund, or via individual companies, is that just 10 stocks are forecast to generate 55% of the FTSE 100’s forecast £62 billion in dividend payments in 2020. Just 20 names are expected to provide 74% of the total. Any UK equity income fund manager will therefore need to have a clear view on all 20 of those names, so they can assess whether the dividend forecasts are right or not, especially with BP right at the top of the list – the oil major is seen by many as primed for cuts to follow that of fellow oil major Shell.

“Just 10 stocks are forecast to generate 55% of the FTSE 100’s forecast £62 billion in dividend payments in 2020. Just 20 names are expected to provide 74% of the total.”

Twenty stocks will dictate the fate of those seeking income from UK equities

Source: Sharecast, consensus analysts’ forecasts

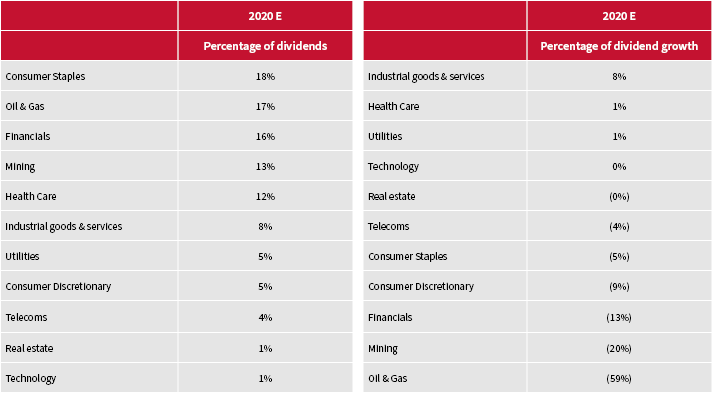

This list inevitably shapes the sector mix of the UK’s dividend payments. Just five sectors are expected to generate three quarters of 2020’s £62 billion in shareholder distributions – consumer staples, oils, financials, miners and healthcare – not least because just three (industrials, healthcare and utilities) are expected to grow their payouts this year. Two of those will only just manage it, if the analysts are right and the industrials rely heavily on a swift return to the dividend’s prior trajectory at BAE Systems and a trio of packaging specialists, Smurfit Kappa, DS Smith and Mondi. Rarely did so much, beyond internet shopping, rest upon containerboard.

Five sectors dominate 2020 dividend payment forecasts

Source: Sharecast, consensus analysts’ forecasts

However, bad news about 2020’s dividend payments hardly represents a surprise after three months of headlines about cuts, suspensions, deferrals and outright cancellations. No fewer than 50 FTSE 100 firms have joined this club, although two – grocer Morrisons and insurer Admiral – only cut special payments and offered ordinary ones while one more – Land Securities – has declared its intention to re-join the dividend list later this year. The fact that 49 FTSE 100 firms have not cut, but aggregate estimates for the total payout have plummeted, only serves to highlight the overall mix of payments by stock and sector.

This takes us to the hoped-for recovery in 2021, when analysts currently predict total FTSE 100 payments will rebound to £75.5 billion, pretty much where they were in 2019.

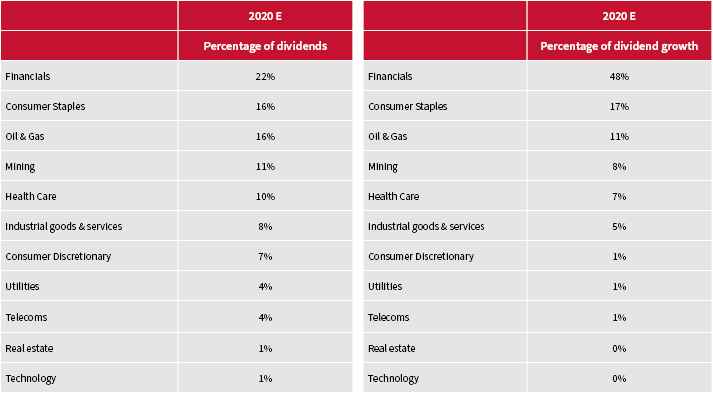

“Two thirds of the forecast increase in FTSE 100 dividend payments for 2021 comes from just two sectors – financials and consumer discretionary, so in essence banks, retailers and insurers.”

The sector mix here is particularly telling when it comes to the source of the anticipated increase. Two thirds of the forecast increase comes from just two sectors – financials and consumer discretionary, so in essence banks, retailers and insurers. Industrials also crop up again, but the rest offer little or nothing.

This could be a source of an upside surprise, should any advisers and clients think inflation is coming and oil and metal prices are primed to rise strongly as a result of a robust economic upturn. Equally, it may be a source of concern, given the pressure the Big Five FTSE 100 banks face from record-low interest rates and Quantitative Easing, which are squeezing net-interest margins, not to mention rising loan impairments, political pressure to go out and lend, the dangers of a slow economic recovery and ongoing regulatory scrutiny. That said, the banks entered 2020 with strong capital ratios and they could return to paying dividends quickly if the recessionary storm passes in short order.

Financials and consumer discretionary dominate the forecasts for dividend payment recovery in 2021

Source: Sharecast, consensus analysts’ forecasts

“The UK does on paper offer an enticing income option for 2021, although advisers and clients may be demanding a juicy-looking dividend yield to compensate themselves for the possible dangers associated with holding FTSE 100 stocks, either directly or via active or passive tracker funds, given the sectoral mix of earnings and dividend forecasts.”

In sum, the UK does on paper offer an enticing yield for 2021. But this assumes that dividend growth forecasts are correct and that key sectors like banks and retailers do the business. Just as is the case with the earnings mix, there looks to be plenty of risk here, as well as opportunity. This may be why advisers and clients are currently demanding that juicy-looking yield to compensate themselves for the possible dangers associated with holding FTSE 100 stocks, either directly or via active or passive tracker funds. And that is before we mention the perceived opportunities and risks relating to Brexit.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.