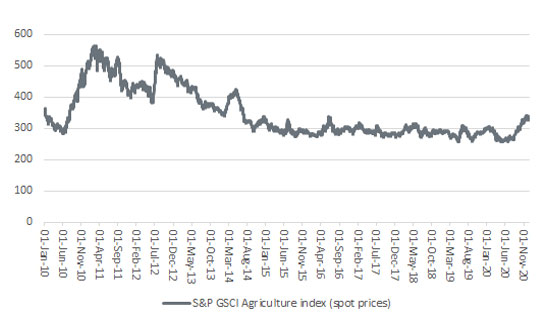

A month ago (Shares, 26 November 2020), this column flagged how commodity prices were rising and how this could be a possible harbinger of inflation, whether it was down to near-term factor such as a La Niña weather pattern or something more deep-rooted. The answer will only become clear with the fullness of time but one trend is worthy of further attention, namely the trend in the S&P GSCI Agriculture index – because if ever a price chart suggests an asset class is breaking a multi-year downtrend, then this could be it.

“If ever a price chart suggests an asset class is breaking a multi-year downtrend, then it just could be the one that shows the S&P GSCI Agriculture index, a benchmark which follows eight ‘soft’ commodities.”

Agricultural crop price index might be breaking a long downtrend

Source: Refinitiv data

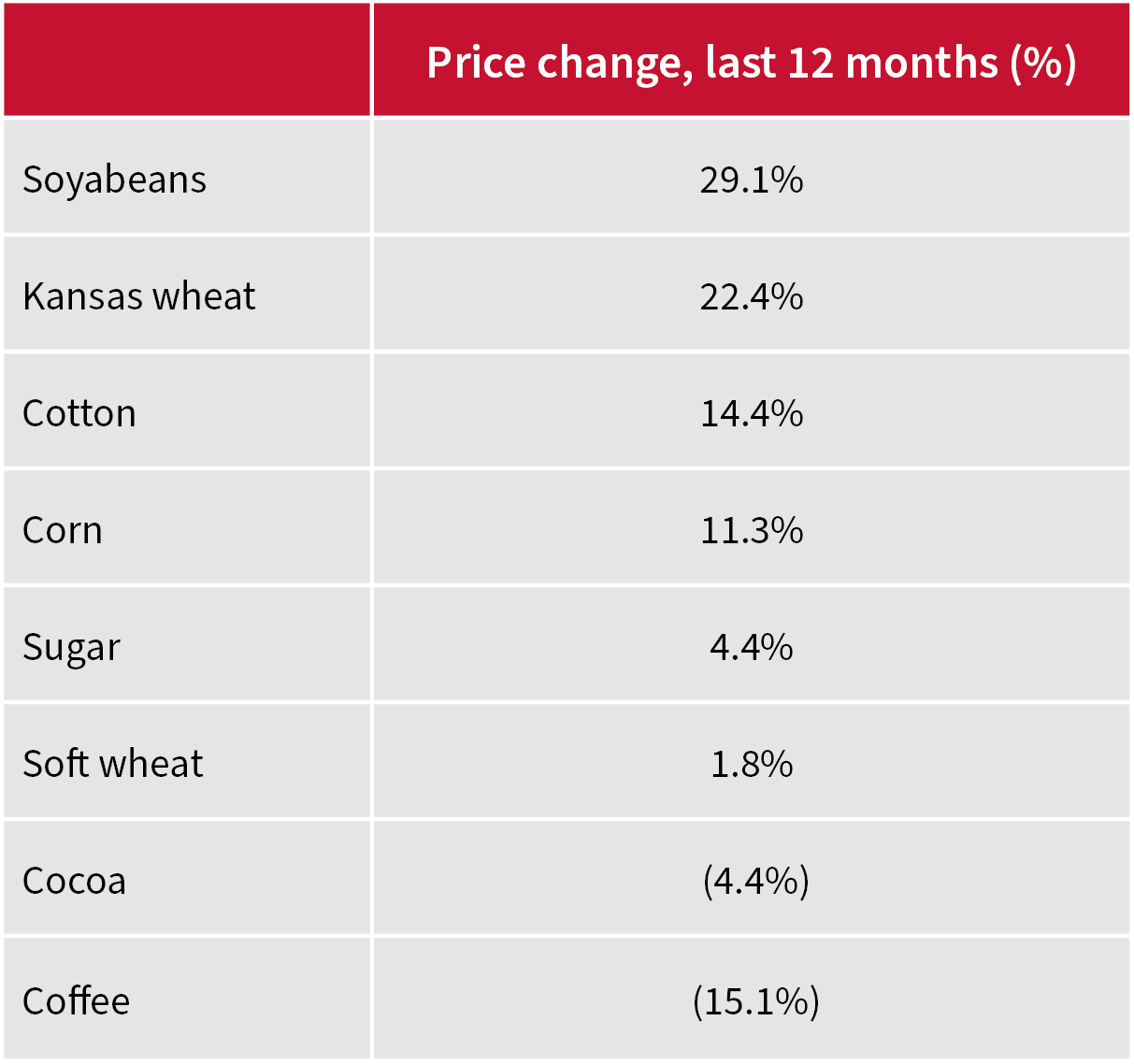

This benchmark follows the price of eight crops, or ‘soft’ commodities – two types of wheat, corn, sugar, soybeans, coffee, cocoa and cotton. For the record, it is soybeans, Kansas wheat and corn that seem to be making the biggest gains. (Cotton prices are also running but, since this column in not in the habit of eating the stuff, it will be set aside for the purposes of this study.)

Soybeans, wheat and corn prices have gone up the most over the last 12 months

Source: Refinitiv data

La Niña’s impact on the unusually dry weather in the US Midwest is one reason why soybeans are so bouncy, along with Chinese buying amid US trade tensions as the country looks to rebuild pig herds after a bout of swine fever. Dry weather in the UK, Ukraine and Romania many explain the strength in wheat prices and the same, La Niña-related phenomenon underpins corn prices as Brazil and Argentina wait on late-developing crops.

All of this suggests that prices could soften as fast as they firmed, especially if the dollar starts to strengthen. Based on the DXY (‘Dixie’) trade-weighted index, the buck is trading near three-year lows just under the 90 mark, but if it rallies, this will make dollar-priced soft commodities more expensive to buy for countries which don’t use the greenback or whose currencies are not linked to it.

“Trade friction between the US and China, US and Europe, Europe and the UK, and elsewhere could be on the verge of reversing the globalisation trend which has facilitated the smooth and increased movement of agricultural products around the world.”

Yet there could be another reason why ‘soft’ commodity prices are firm in so many cases. Trade friction between the US and China, US and Europe, Europe and the UK, and elsewhere could be on the verge of reversing the globalisation trend which has facilitated the smooth and increased movement of agricultural products around the world. Foodstuffs may not have been the main reason for the tensions but tariffs have been applied in many cases all the same and those levies and taxes have presumably served to increase end-market prices, too. In this context, the warning from Tesco that food prices could increase by 5% in the event of a ‘no-deal’ Brexit is worth bearing in mind.

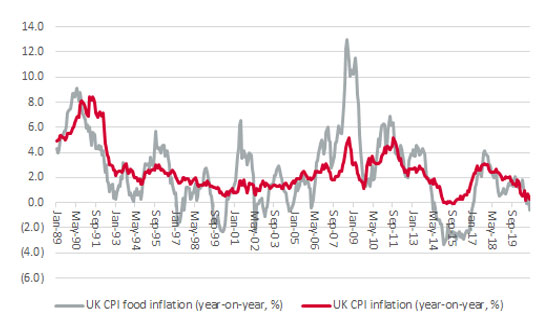

A deal could still ease any such worries but the break in the downward trend in global food prices is eye-catching all the same. The good news is that, in the latest UK inflation figures (15 December), food prices fell by 0.6% on average year over year, helping to anchor the headline consumer price index (CPI) inflation rate at 0.3%. But if food prices do suddenly take off, history suggests that the headline rate could catch light, too, a development which neither central banks nor financial markets seem to be expecting.

UK food price inflation is still subdued…

Source: Office for National Statistics

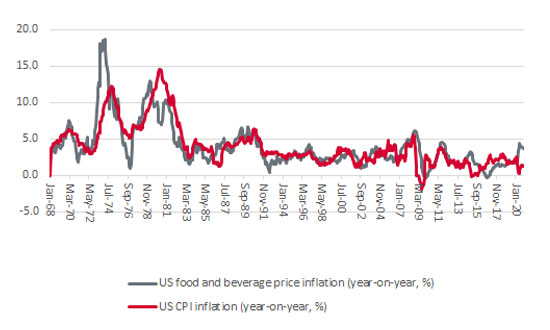

… but it seems be gathering pace in the US

Source: Office for National Statistics

Intriguingly, however, the latest food and beverage price inflation rate in the US was 3.7%, miles ahead of the benign headline figure of 1.2%. Looking at the long-term US data, which has a longer available history than the British version, it could be argued that where food price inflation goes, then the headline US consumer price index inflation rate looks pretty sure to follow.

“Food price inflation might be a nasty surprise to US consumers (and British ones if they end up with the same trend), whether this is down to La Niña, nationalism, tariffs or something else.”

This might be a nasty surprise to US consumers (and British ones if they end up with the same trend), whether this is down to La Niña, nationalism, tariffs or something else. It could be the sort of trend that triggers demand for higher wages. Whether labour feels sufficiently empowered to put its foot down right now, as unemployment ticks higher thanks to the pandemic and the economic damage wrought by lockdowns, is admittedly debatable.

Any historian will tell you that food prices may not be the cause of revolutions or public uprisings but they can be the trigger for them, with France in 1789, Tiananmen Square in 1990 and the Arab Spring in 2011 as examples of this. This column is not suggesting that geopolitical turbulence will result but, from the narrow perspective of financial markets, any sustained bout of inflation would be a major revolution of a different kind.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.