Fund pickers differ in philosophy and process, but one common theme we see across the board is applying a minimum size a fund has to be before it can be used in portfolios. Sometimes it is £50 million, often it is £100 million and, if you are based in France, it may be €100 million!

On the surface, this application of a minimum fund size seems arbitrary. A fund is not necessarily a bad fund at £90 million; equally, if a fund reaches £110 million, it is not suddenly a better proposition. However, the application of a minimum fund size in the active fund world makes sense – it helps weed out the ones that are likely to underperform, which in turn may lead to closure. It also helps to navigate the regulatory framework, such as UCITS.

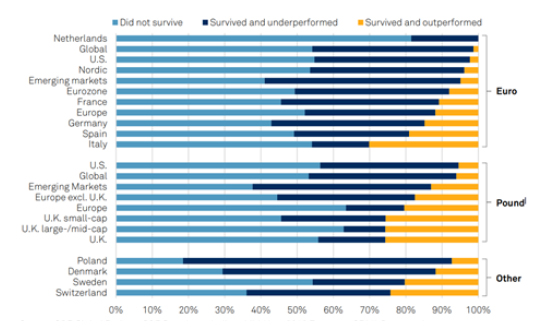

Data from S&P shows how few active funds have outperformed their index over the last decade and, perhaps more surprisingly, how few funds actually survive. For example, for UK equity funds, around a quarter outperformed their index and less than half survived the full 10-year analysis period.

European equity funds: Survivors and outperformers, survivors and underperformers, and those that closed, June 2009-June 2019

Source: S&P Ratings, S&P Dow Jones Indices mid-year 2019 European SPIVA scorecard

So why would a minimum fund size help you to avoid the losers? In a word: costs.

These can be costs passed on directly to investors such as administration charges – the smaller the fund, the higher these costs are as a proportion of the fund.

Costs also have a more subtle effect on a fund’s longevity – the larger the fund, the larger its revenue stream, covering fixed overheads and allowing it to reinvest in improving its process. The smaller the fund, the less likely it is to outperform, or even survive. It is clear that setting a minimum increases your chances of picking a manager with lower costs, a solid process and which will be around for the years to come.

As ETFs and passive investing have grown, these same fund pickers have been charged with picking ETFs and index-tracking funds. The same minimum used as part of the active process is therefore often applied for picking passive investments: we challenge this notion, and explain how we think about this for ETFs.

A passive product aims to track an index; it does not rely on a star manager or a team of research analysts generating ideas. It instead relies on a combination of technology and a team focused on ensuring the fund replicates the index as closely as possible. It operates with a fixed ongoing charge, with the fund manager absorbing all variable charges. As such, a significant number of the costs and challenges with an active fund disappear. But not all of them.

With the exception of Vanguard, all passive managers are in the business of making a profit. As such, like an active manager, its proposition needs to be viable. The higher its revenues, the more it can invest in the technology that ensures products track efficiently. The key difference here is that it is the viability of the ETF manager that is more important, rather than the individual products, which all run off the same technology and use a team of portfolio managers. We saw this in 2019, when BMO stepped away from the European ETF market, after failing to build critical mass despite its Global High Yield Bond ETF gathering assets of more than £100 million. Growing an ETF operation may also be a business hedge for large active managers, so this changes the requirement to make a short-term profit.

There is no rule of thumb here – especially given that some ETF products are high margin and others are likely loss-making – however, as part of our process, we gather information directly from the provider to understand its commitment to the market: once a provider has billions rather than millions under management, its position in the market is cemented.

This is not to say a smaller ETF manager cannot be successful, but it does carry additional risks, especially given the resources required to distribute into a fragmented European market.

However, this does not mean you shouldn’t consider the size of the individual ETF when you are making your choice. It is, however, a much more nuanced assessment, combining size with qualitative elements. When deciding which ETFs we use, we focus on three key areas to understand if the product is big enough, discussed in detail below.

All products need to be large enough that they are able to build a diversified portfolio that will track its index closely. For equity ETFs tracking well known indices such as the FTSE 100, the minimum is in the low millions. The manager can access a liquid futures market to stay fully invested and individual shares can be bought to maintain index weights.

As the equity product becomes more complex, such as factor tilts or investing internationally, these minimums increase. For example, in emerging markets, it allows the provider to access global depositary receipts if the fund is bigger – however, this is still significantly below the £100 million minimum often used as a rule of thumb.

When investing in credit ETFs, these minimums can be larger as the underlying bonds often trade with £100,000 minimums, and a larger number of bonds is required to effectively track the index. When we invest in a smaller credit ETF, we ask the provider to explain what size is required to track well and then we build in a margin of safety.

Unfortunately, there is not a one-size-fits-all approach here, as using a blanket minimum precludes an investor from using a product that may be cheaper and contain additional features, such as liquidity screening. We set a different minimum for equity ETFs and bond ETFs based on our assessment of ability to track, however we do not rule out smaller products as we feel it is important to encourage competition in the market. Without this stance, the big products just get bigger, leading to little price competition, and innovative products do not gain traction – a negative for users of ETFs.

One of the key features of ETFs compared to index funds is the ability to trade on the secondary market, offering an extra liquidity valve.

Given this feature sits alongside the traditional primary trading mechanism – meaning trading costs are linked to the cost of trading the underlying securities – we do not think access to the secondary market (or lack thereof) should preclude the use of an ETF in a portfolio.

The amount invested in an ETF is loosely correlated with the depth of its secondary market, however the link is not as strong as you may think. For example, many Vanguard products have steady buying activity, meaning a lot of volume ends up on the primary market, whereas Blackrock products, although experiencing longer-term asset growth, are often used as short-term trading instruments, as we saw during the March 2020 drawdown, leading to a deeper secondary market.

The more liquid the secondary market, the more likely the ETF will offer a spread improvement compared to the underlying securities, so looking at bid/ask spreads of the ETF is more important than looking at the size. Even then, the majority of ETF trading is done over the counter, with the exchange prices not reflective of where trading would be executed.

However, it is worth noting that smaller products often have contracted market makers to control spreads, and can often trade more tightly than larger products. In addition, a larger product may see more sentiment-driven buying or selling, which may lead to higher volatility in its price premium or discount – this is especially true of physically-backed UK equity trackers, given the application of SDRT on share purchases, which often drives the ETFs to a 0.5% premium when there is net buying, but back down to fair value when there is prolonged net selling.

Therefore size is loosely linked to how easy the ETF is to trade, but it is much more complex when you dig into the weeds. Instead, spreads and the stability of the premium and discounts are better indicators.

In 2019, we saw an increase in de-listings of European domiciled ETFs, so it is important not to ignore the chance a product will be discontinued. However, as we have already touched on, this is often down to the viability of not just the product, but the ETF manager as well.

The providers look to offer a full range of solutions, so even if the UK equity ETF of a provider is on a small scale, it is an important part of its toolkit to its UK based investors, and as such is likely to remain even if it is loss-making as a standalone proposition – the manager is aiming to provide a one-stop shop, and with the exception of Vanguard, we suspect all providers operate ‘loss leaders’.

The market is evolving quickly and asset classes come in and out of fashion; it is therefore important that providers have a product available to take advantage of any macro shifts, such as those seen in the recent drawdown when investors flooded to gold ETCs.

However, we try to treat a small niche ETF combined with declining assets with caution. We assign a higher asset hurdle when looking at strategies following more complex strategies, such as thematics. The flavour of the month may quickly become a thing of the past.

Putting this altogether into a simple framework is complex, however we try to distil this into a set of rules when selecting ETFs.

By using this framework rather than using arbitrary product minimums, we are able to access better products earlier – making sure our portfolios represent good value to investors – and keep competition within the industry high – which is a benefit to all ETF users.

If you want further information on the AJ Bell passive MPS or Funds, please contact your Business Development Team.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.