There is a phrase in business called ‘Shrink to greatness’, meaning the action by companies to sell or demerge assets and focus on what they do best.

You might call it streamlining, others might say it is an admission that the previous strategy did not work and the company was too bloated. Whichever view you take, the trend is firmly in motion across the UK stock market, with 9 companies in the FTSE 100 either in the middle of shrinking or having recently done it.

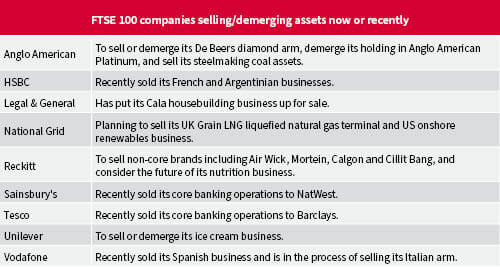

For example, Reckitt has put certain well-known brands up for sale and Unilever is separating its ice cream arm from the rest of its business. There are further FTSE 100 companies ripe for getting rid of non-core assets including Diageo and WPP.

FTSE 100 companies selling/demerging assets now or recently

Source: AJ Bell, Company announcements

A falling share price, pressure from activist investors to enact change, or fighting off a takeover attempt are three key catalysts for a company to ‘shrink’ through asset sales or demergers.

Investors unhappy with share price performance often call for a business to sell certain assets in the hope they are worth more than the market attributes. This can range from selling property at greater than book value to selling operating divisions that certain investors did not even realise existed or held any value of note.

ITV surprised the market in March by selling its stake in the international part of its Britbox streaming venture for £255 million. Most people thought Britbox was a disaster and worth nothing, not 11% of the entire market value of ITV, which turned out to be the case. ITV’s share price has pushed ahead since this sale as investors wonder what else has hidden value inside the group.

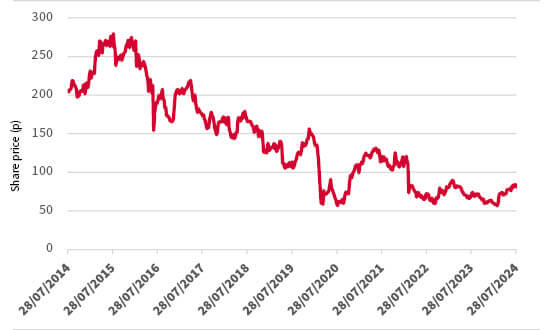

Source: LSEG

Despite the pickup in the company’s valuation in recent months, the shares are still trading 70% below their peak in 2015. The market continues to fret about the broadcaster’s exposure to traditional (linear) TV, where viewing trends are in decline across the industry.

That is the bad, but what about the good? Certain fund managers believe the ITV Studios production arm is worth more than implied by the group’s market valuation. The ITVX streaming platform is also making progress and there are brighter prospects ahead for advertising income as ITV can offer more information on viewers – data which is valuable for companies seeking targeted promotions.

ITV has so far rejected the idea of selling the Studios arm to realise hidden value. That looks a sensible call given it is crucial to the group’s success as it feeds a range of ITV’s own broadcast channels and streaming platform with content, and also generates good revenue from licencing fees.

Elsewhere, who knew FTSE 100 life insurer Legal & General owned a housebuilder? Most people did not until it put the business, called Cala Homes, up for sale earlier this year with a reported £750 million price tag.

Unilever no longer wants to sell ice cream. Even though it owns widely-loved brands such as Magnum, Wall’s and Ben & Jerry’s, the division has lower growth prospects than the rest of the group.

In theory, exiting this product line should improve the growth profile of Unilever and potentially lead to investors being willing to pay a higher multiple of earnings for the shares. That is the plan, but there is no guarantee it will play out in such a way.

Reckitt is going to sell various brands which certain people thought were among its crown jewels – including Air Wick, Europe’s biggest air care brand; Calgon, Europe’s biggest water softener brand; and Cillit Bang, Europe’s fourth-biggest surface cleaning brand. These are iconic products and Reckitt should not struggle to find buyers.

Why is it offloading them? It is the sign of a new chief executive trying to make their mark and distance the business from mistakes of old. Reckitt’s share price is trading at an 11-year low, thanks to worries about the quantum of liabilities from legal action around a baby formula product and from longer-standing concerns about strategic mistakes.

Source: LSEG

If you were digging around the house looking for things to sell, it is easy to pick items that you know could fetch a decent price alongside other items you no longer want. There might be elements of this approach with Reckitt, alongside a bigger strategic move to sharpen its focus and do fewer things.

It wants to concentrate on the brands that generate the most profitable business for the group. Reckitt might also sell the nutrition business housing the baby formula products once its resolves legal issues.

Demergers can be one way to appease shareholders who wish to maintain exposure to a specific part of a business but where there is a ‘shrinking’ strategy in motion. Shareholders in the parent company receive free shares in the demerged entity, which they can either keep or sell on the market.

The FTSE 350 index is full of companies born out of a demerger. For example, miner Anglo American spun off packaging group Mondi, drug company Haleon used to be part of pharmaceutical giant GSK, and engineer Dowlais was previously a division of Melrose.

It is worth keeping an eye on demerged entities as they might flourish once they have left their former parent. This is often the result of management being free to make their own decisions rather than the parent company dictating them.

A study in 2003 by the Krannert School of Management found that subsidiaries spun out of companies outperformed their former parent by more than 20% over the first three years following the demerger; with a majority of the excess returns within the first 12 months of trading.

This chimes with a US tracker fund designed to mirror the performance of companies spun off from larger corporations within the past four years. The Invesco S&P Spin-Off ETF is up 23.9% over the past 12 months versus 12.9% from its Russell Midcap index benchmark. Over three years, it is up 4% versus 2.4% from the benchmark.

Those periods are too short-term to draw any firm conclusions and investors must appreciate that past performance is not a guide to future performance.

Selling assets or spinning off parts of a business might make the original parent company’s profit margins look better for a while, but investors will always be looking for new growth catalysts.

Once the ‘shrinking’ has played out, a chief executive will be under pressure to take the business forward and that eventually raises the temptation to do deals to accelerate growth. A company which had slimmed down might easily fatten up again. It is just the nature of business.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.