Bruce Kovner may not be the best-known hedge fund manager in the world but, as the founder of Caxton Associates, he is one of the most successful. He gives little away in public, but it is worth tracking down his few pronouncements and one of this column’s favourites is his comment, “What I am really looking for is a consensus the market is not confirming.”

Right now, so far as this column can tell, the consensus is that oil prices are going to stay high, either because OPEC+ will maintain supply discipline, or because oil firms are wary of big new drilling projects (because of environmental or political pressure or both), or because of the war in Ukraine, or perhaps a combination of all three.

“So concerned is World Bank President David Malpass about oil prices that he is citing the Russian invasion of Ukraine, and its effect upon commodity prices, as a potential cause of a global slowdown, if not an actual recession.”

So concerned is World Bank President David Malpass about oil prices that he is citing the Russian invasion of Ukraine, and its effect upon commodity prices, as a potential cause of a global slowdown, if not an actual recession.

Oil stocks are responding to this environment. Shares in Shell (SHEL) and BP (BP.) are both back to pre-pandemic levels and Shell is nudging toward its prior all-time peaks (even if BP is some way short of that).

“But when oil stocks are studied in a wider context, it seems as if investors do not really believe that crude will remain in the ascendent for too long, possibly in the view that the long-run move away from hydrocarbons to alternative, renewable sources of energy is still on track.”

But when oil stocks are studied in a wider context, it seems as if investors do not really believe that crude will remain in the ascendent for too long, possibly in the view that the long-run move away from hydrocarbons to alternative, renewable sources of energy is still on track.

Whether this is a good example of a situation where share prices remain sceptical of what seems like the consensus is something that investors can only decide for themselves, but managing the transition from oil and gas to wind, solar and others may yet take time.

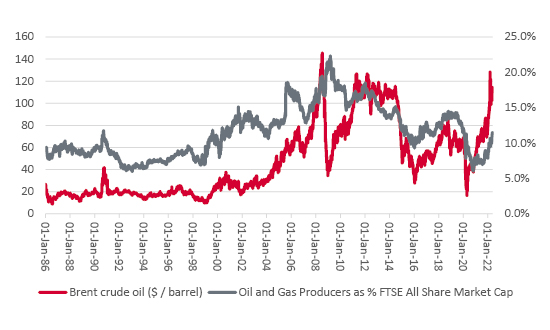

It is therefore interesting to note that oil stocks still represent only 11.4% of the FTSE All-Share’s market capitalisation, compared to historic highs north of 20%, when oil also traded consistently above $100 a barrel.

UK oil stocks remain of diminished importance in the UK equity market

Source: Refinitiv data

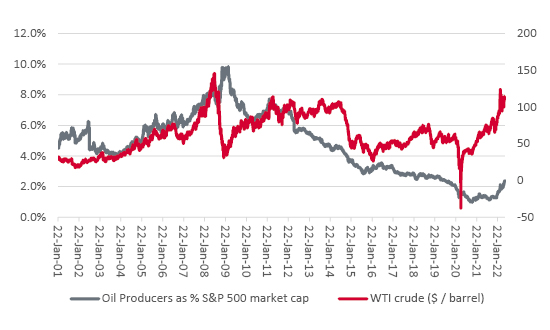

Oil stocks also seem to be relatively out of favour in the USA, where their profile, as measured by their percentage of the overall stock market’s valuation, is still languishing near historic lows.

“In the USA, the major oil producers command an aggregate market capitalisation which represents just 2.4% of the S&P 500 index’s total $33 trillion price tag. Granted, that is a big leap from the lows of autumn 2021 but it is barely a quarter of the highs seen in the middle of this millennium’s first decade.”

In the USA, the major oil producers command an aggregate market capitalisation which represents just 2.4% of the S&P 500 index’s total $33 trillion price tag. Granted, that is a big leap from the lows of autumn 2021 but it is barely a quarter of the highs seen in the middle of this millennium’s first decade.

US oil stocks also have a much lower profile relative to historic averages

Source: Refinitiv data

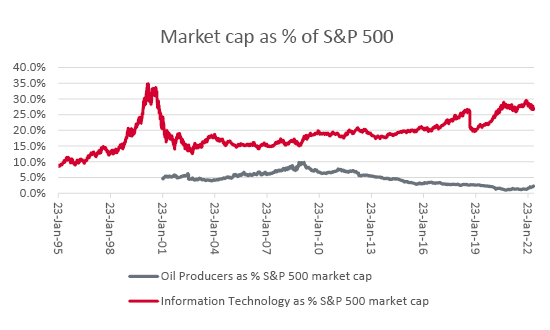

This is in stark contrast to the market’s apparent ongoing love affair with technology stocks. The US Information Technology sector did not quite reach its prior peak at around 35% of total S&P 500 market cap this time around. That may be no bad thing, given how badly that 1998-to-2000 surge came to grief in 2001-to-2003’s bear market, but tech still reached 30% during the pandemic as some investors decided it was the only story in town. Tech’s loss of favour may feel uncomfortable for many, but its reversal of fortune still looks minor compared to the rout of twenty years ago.

Tech still carries a hefty market weighting in the USA

Source: Refinitiv data

This takes us to another money management legend, Bridgewater’s Ray Dalio, who is less circumspect when it comes to expressing his views publicly than Mr. Kovner. One pearl from Mr. Dalio is this: “The biggest mistake that investors make is to believe that what happened in the recent past is likely to persist. They assume that something that was good investment in the recent past is still a good investment. Typically, high past returns simply imply that an asset has become more expensive and is a poorer, not better, investment.”

The crunching falls in many tech stocks would perhaps lead investors to think the consensus is bearish, just as oil shares’ ongoing resilience, even in the face of the UK’s 25% windfall tax, would give the impression that everyone is bullish on oil stocks.

The historic trends given to these sectors, and their relative weightings now, would suggest that may not be the case. Tech still feels loved, oils still feel reviled.

Such a view may be borne out over time, and this column has no crystal ball with which to confirm or contradict current trends. But the UK Government is now introducing its third piece of legislation that can only sustain demand for oil and gas, in the form of the discount on energy bills for all and further support for less affluent households. This follows the subsidies for domestic air travel and cut in fuel duties.

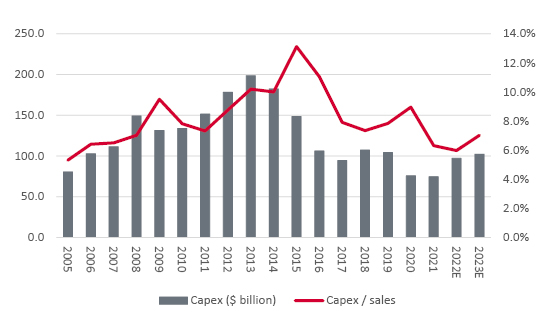

“That stimulus, or ‘stimmy,’ comes when supply is already tight relative to demand, as banks, insurers and fund managers decline to offer finance for new exploration work and the Government threatens any successful risk-taking with more tax. Not surprisingly, oil majors’ capex is nearer its lows than cyclical highs.”

That stimulus, or ‘stimmy,’ comes when supply is already tight relative to demand, as banks, insurers and fund managers decline to offer finance for new exploration work and the Government threatens any successful risk-taking with more tax. Not surprisingly, oil majors’ capex is nearer its lows than cyclical highs.

Oil majors are still being careful with their capex plans

Source: Company accounts, Marketscreener, for BP, Chevron, ConocoPhillips, ENI, ExxonMobil, Shell and TotalEnergies.

This could be bullish for oil and the consensus seems to agree, even if share prices and valuations appear less convinced. Over to you, Mr. Kovner.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.