The first quarter of 2025 was always expected to bring significant noise from the new US administration; however, no one knew exactly what it would mean for the markets. The pace and scale of executive orders signed after the inauguration quickly left markets and companies scrambling to keep up with developments. This, in turn, led to heightened scrutiny of the US economy, the equity market, and the dollar. Bond markets also had to assess the implications for growth against a backdrop of persistent, above-target inflation.

In the US, concerns over indications of a sudden deterioration in economic growth – based on the Atlanta Fed’s economic forecasting model – along with rising uncertainty around trade policy, brought rate-cut expectations into sharper focus as the quarter progressed. On one hand, tariffs posed an inflationary threat; on the other, early signs suggested that businesses were delaying spending plans, which could have a deflationary effect. This shake in confidence caused the US dollar to fall sharply against major peers and Treasury bond yields to decline across the curve.

Conversely, continued inflationary pressure in the UK, coupled with early warnings of utility price increases in the spring, suggested that the Bank of England (BoE) might need to keep interest rates higher for longer. After surging bond yields at the start of the year, a period of relative calm was disrupted in the run-up to the Spring Statement, as concerns over fiscal sustainability resurfaced. Across corporate bond markets, credit spreads in the US began to widen from particularly tight levels, though not enough to offset coupon payments.

Source: AJ Bell, 01/01/25 to 31/03/25. Total returns represent those in local currency terms.

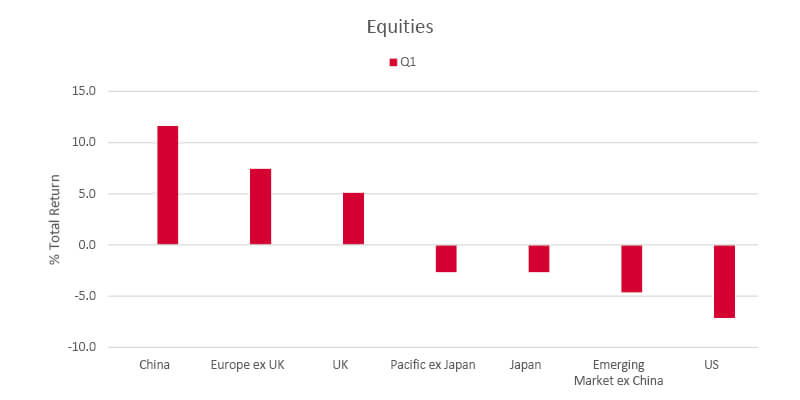

Equities experienced significant dispersion in the first quarter, with most regions outperforming the US market – contrasting with the trend of the past couple of years. As part of this shift, the so-called ‘Magnificent 7’ reversed course. Tesla, in particular, suffered from trade uncertainty with China and Europe, as well as unease over its co-founder’s association with policies unpopular with the typical Tesla customer.

Meanwhile, in Europe, the so-called "debt brake" in Germany was reformed as part of post-election negotiations, paving the way for potentially significant spending on infrastructure, defence, and the energy transition. Investor sentiment had been weak heading into 2025, and this unexpected development triggered a significant rally across European equities.

Turning to another previously underperforming equity region, China, the year started strongly as AI technology emerged as a challenge to US incumbents. Alongside this, positive government overtures toward tech companies led to a rally in H-shares listed in Hong Kong.

UK equities had a solid start to the year, benefiting from the sector diversification of the UK market. The energy and financial sectors performed well, with banks seen as benefiting from the higher-for-longer interest rate environment.

Source: AJ Bell, 01/01/25 to 31/03/25. Total returns represent those in GBP terms

The economic impact of the shifting global trade landscape is yet to be seen, and the jury is still out on whether this will trigger a US recession in the near term and, by extension, a global recession. This likely depends on whether tariffs are being used as a negotiating tactic to bring trading partners to the table. A case in point is Europe and China, which would seemingly prefer to avoid a global recession that could disrupt their efforts to boost domestic growth – efforts that, in themselves, are likely to remain a focal point as the year progresses.

The value of investments can go down as well as up and your client may not get back their original investment.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.