The use of outsourced investment management services has created a potential challenge in defining the relationship between advisers, discretionary fund managers (“DFMs”) and ultimately their relationships with the end investor in advising on and managing investors’ interests. In this article, we will explore the operating models available within adviser / DFM agreements and the potential consequences for advisers in the adoption of either option.

It is important to note that both operating models discussed within this article offer advantages and disadvantages, with no ‘right’ or ‘wrong’ way to structure DFM / adviser relationships; the most suitable framework will depend on the specific circumstances of an adviser’s firm and their relationship with their clients.

The pace of important regulatory change in recent years, initially through the introduction of MiFID II and the Asset Management Study, ushered in specific requirements in the manufacture and distribution of investment products (as captured within PROD). The principles of the Consumer Duty have further broadened, codified, and sharpened the emphasis on firms in the ongoing monitoring and oversight of arrangements made on behalf of investors’ interests.

This has all duly increased the burden on adviser firms to have sufficient expertise and resources to support the running of in-house model portfolios, where they have their own discretionary permissions.

The trend within the UK industry in the use of multi-asset strategies and third-party DFMs looks set to continue as advisory firms look to serve their client base as effectively, and efficiently, as possible. It is therefore important to understand the operating model so that an agreement can be made between an adviser and DFM, and vital that all parties involved understand the practical implications along the distribution chain in managing investors’ interests.

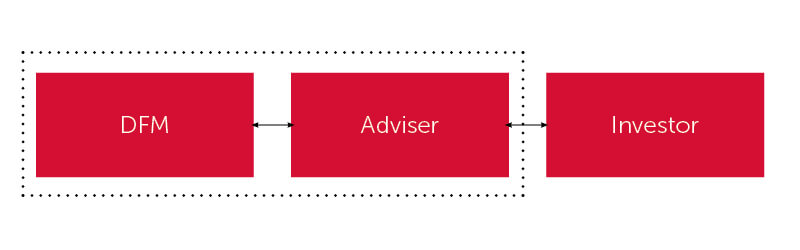

The two most typical scenarios are ‘Agent as Client’ (AAC) and ‘Reliance on Others’ (ROO).

With an AAC arrangement (see COBS 2.4.3R), the investor’s ‘agent’ – their adviser – is fundamentally the client of the DFM. The adviser arranges for the underlying investor’s portfolio to be managed by a DFM, with no direct contractual relationship in place between the investor and the DFM. Rather, the investor’s adviser (the ‘agent’) holds the relationship with the DFM.

An AAC arrangement is shown in the diagram below, with the dashed line representing the DFM’s client relationship with the adviser; this does not extend to cover the investor.

ROO (see COBS 2.4.4R) is an alternative operating model where the underlying investor has a direct, contractual relationship with the DFM and, in turn, the DFM relies on the information provided to it by the investor’s adviser.

The below illustrates the tripartite relationship in place under the ROO operating model.

Operationally, there may seem like there are very few differences between AAC and ROO – certainly from the perspective of an underlying investor. However, these differing regulatory structures do have various implications for all parties involved and their responsibilities. One important example is suitability.

Under an AAC arrangement, the adviser is responsible for the mandate and also the investment management under that mandate. This means that a complaint from an investor under an AAC arrangement may not be able to be brought against a DFM, and the adviser would instead be liable.

A perceived advantage of the ROO model is that it clearly defines the responsibilities of the adviser and the DFM in the services that they are providing to the end investor. The adviser retains the responsibility of assessing suitability of a product for a client, as well as retaining the relationship, whilst the DFM relies on this recommendation of suitability and is responsible for delivering the investment mandate to the investor through the managed portfolio service.

As a result of the subtle differences within the model structures, there are potential consequences here in terms of risk and insurance cover for an adviser, which would need to be carefully considered.

Advisers should therefore analyse, alongside their DFM and PI insurer, whether the appropriate paperwork and oversight procedures are in place to ensure robust compliance with regulatory requirements and the most critical consideration of all – ensuring the best outcome for underlying investors.

AJ Bell Asset Management (AJBAM) operates on a ROO basis for the DFM services it provides through its Managed Portfolio Service and Partner MPS ranges, distributed through the AJ Bell Investcentre platform. For the Partner MPS service, AJBAM and a suitable adviser firm are both co-manufacturers of the portfolios, which are specifically constructed for the adviser firm’s investor base.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.