If you blinked, you might have missed it, but there was a flicker of life in the UK stock market in July. The FTSE 250 index of medium-sized companies jumped by almost 4% in one day, its best showing for over a year. In and of itself this isn’t too remarkable; markets rise and they fall, capriciously and sometimes sharply. But this little spike might be worthy of some more attention, because of what prompted it: inflation. Or to be more exact, falling inflation. On 19 July, the latest reading of the Consumer Price Index showed a drop from 8.7% to 7.9%, more than city analysts expected. Domestic stocks soared on the news, with shares in some housebuilding stocks jumping by 10%. Inflation remains way outside everybody’s comfort zone, and that’s still problematic. But this little episode shows that there may be some pent-up energy trapped inside the UK stock market after all.

UK investors will be hoping that this might mark an inflection point, when markets finally start to believe that UK shares are oversold.

UK investors will be hoping that this might mark an inflection point, when markets finally start to believe that UK shares are oversold. A recent research note from the fund managers of Temple Bar investment trust suggested there was a compelling case for investors to consider re-balancing away from US equities and towards international equities, and in particular UK equities. This is perhaps not too surprising a viewpoint from a trust that invests predominantly in UK shares, but certainly the domestic stock market has been deeply out of favour for some considerable time.

While it’s posted decent absolute returns so far in 2023, the FTSE All Share has lagged behind international peers, especially the powerhouse that is the S&P 500. The July fillip in share prices has put it back in the race, but it’s still at the back of the pack. That might be easier to swallow if it didn’t come on the back of a pretty disappointing longer term run. According to Morningstar data, over 10 years the UK stock market has returned 72%, compared with 103% from the Japanese market, 110% from the European stock market, and a gasp-inducing 267% from the S&P 500 in the US, all in sterling terms. Little wonder then, that UK fund managers think it’s about time for some sunnier weather for UK stocks.

Global markets % total return in 2023

SOURCE: Morningstar total return in GBP

Despite the valuation gap, an aversion to the UK has been a long-running theme, and it’s been evident within both private and professional investor portfolios.

The valuation of the UK stock market also looks attractive, especially when set against the US. The Price Earnings ratio of the average stock in the FTSE 350 is currently sitting at 12.7 times the next 12 months of estimated earnings, compared to 18.5 times for the S&P 500, according to Refinitiv data. It’s important to bear in mind that the UK and US stock markets have a very different sectoral make up though, and the old economy stocks which make up so much of the Footsie, like banks and mining companies, are expected to have a lower long-term growth trajectory than the technology stocks that sit atop the S&P 500. This goes a long way to explaining the divergent valuations placed on the two stock markets.

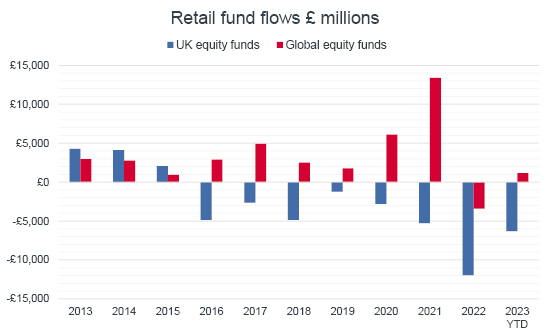

Despite the valuation gap, an aversion to the UK has been a long-running theme, and it’s been evident within both private and professional investor portfolios. Retail investors have pulled £40 billion out of UK equity funds in the last seven and a half years. Given the rot started in 2016, it’s hard to escape the conclusion that Brexit played a major part in triggering the exodus. There are other factors at play too though. Investment flows have been affected not just by a push from underperforming UK equities, but also by the pull of global shares, especially in the US where technology stocks have shown a clean pair of heels to other sectors. UK investors could also be forgiven for unwinding a large portfolio position in UK equity funds, which has naturally become more diversified as the investment industry has provided more international funds for investment.

Retail fund flows £ millions

SOURCE: Investment Association

Even within the global funds which have proved so popular in the last few years, the allocation to the UK has been dwindling. This is mainly because the poor relative performance of UK shares, especially in comparison to the US, has reduced the proportion of the global market made up by UK companies. Hence why a global tracker fund has gone from holding 9% in UK equities ten years ago to just 4% today. Global active funds have kept the faith a little more, but have on average still substantially reduced the proportion they’re willing to invest in the UK. These active managers are still benchmarked against the global stock market, and so can’t keep much more invested in the UK without increasing their risk of underperformance.

% of global funds held in UK equities

SOURCE: AJ Bell, Morningstar

If inflation continues to fall in the UK, we could see a bit more of a bump in the stock market.

It’s possible these trends will abate, or even reverse, but it’s by no means certain, especially seeing as it will take time for any better performance from the UK stock market to meaningfully turn the tide of investor sentiment. Market trends can be deeply entrenched for long periods; just ask anyone investing in Japan in the nineties and noughties. If inflation continues to fall in the UK, we could see a bit more of a bump in the stock market. Even so, investors who want to take a contrary view to the prevailing antipathy towards the UK do need to be patient, and willing for things to get worse before they get better. Though one thing you can’t argue is a feather in the cap of the UK stock market is the prevalence of dividend paying companies, with the FTSE 100 forecast to yield 4.4% in 2024. So at the very least investors are being paid to wait for a turnaround.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.