Investing with patience is like hiking up a mountain – it can be tempting to sprint forward on flatter ground or chase side paths that look exciting in the moment. But rushing or losing focus can waste energy and lead you off course. The real progress comes from keeping a steady rhythm, taking one sure step after another, adjusting when the trail truly turns, and ignoring any false way markers. Instead of trudging sluggishly, you’re moving with intent and conserving strength for the steeper climbs ahead. And while others may veer off the path or burn out too soon, you arrive at the summit with clarity, and the ability to enjoy the view.

This hike is what we’re trying to achieve with our Strategic and Tactical Asset Allocations (SAA / TAA). The SAA sets the direction of travel needed to reach the summit, the TAA is like a map check along the way.

Our check of the map heading into 2025 revealed a few rocky outcrops to be aware of.

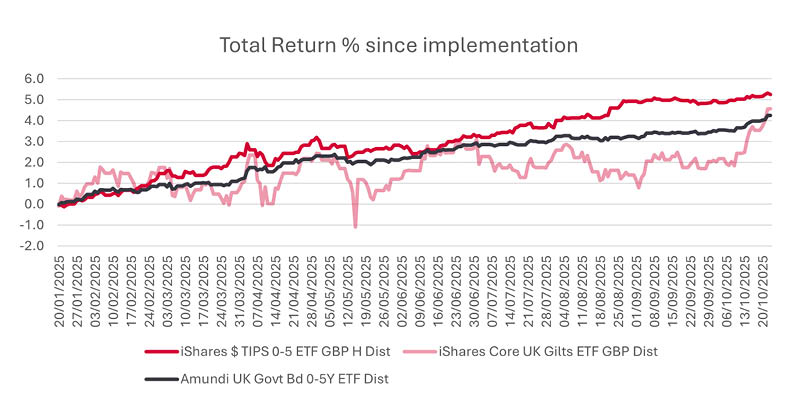

In our view, longer-dated bonds faced an inflation problem that might make progress tough going. In response, we shortened portfolio duration in January, and added protection in the form of shorter-dated US TIPS at what we thought were attractive real yields.

Elsewhere, the market cap approach to equities had seen concentration rising, with returns in 2024 driven by a select few stocks in the US. Although it could have become worse, and indeed it has, we saw enough to suggest the market may behave differently to what its historical volatility might suggest (historic volatility is a key input of our SAA).

Looking down at our map in the fourth quarter of 2025, as we have done at several previous points throughout the year, our assessment is that we are on the right path.

Inflation has returned as a theme of 2025, and markets are tentatively becoming more aware of the issues and risks in bond markets. For portfolios, this means we’ve been able to add value via our fixed-income TAAs so far this year, over and above that of the SAA performance. Crucially, it has also allowed us to provide a smoother journey.

As a reminder, the AJ Bell Cautious and Moderately Cautious funds (alongside MPS 1 and MPS 2 across the MPS ranges) have spilt allocations between standard-duration gilts, short-duration gilts and short-duration US TIPS (hedged back to sterling). Whilst the AJ Bell Balanced fund (MPS 3) is allocated solely to US TIPS, the AJ Bell Cautious fund (MPS 1) has some exposure to shorter-dated US Treasuries that aren’t hedged back to sterling.

Source: Morningstar Direct, Total Return in GBP from 20/01/2025 to 23/10/2025. No rebalancing impact is assumed and therefore this does not represent actual portfolio level performance. The AJ Bell funds mostly use direct bond holdings rather than ETFs for these allocations.

2025 has brought several new developments that are supportive of our views on inflation.

The vulnerability of the UK to higher inflation is being revealed in 2025, as a rise in goods prices has built upon sticky service sector inflation. The gilt market has been on edge at times when it comes to fiscal policy, however, more recently it has responded positively to a slightly-better-than-expected September CPI (flat at a year-on-year rate of 3.8%). Despite the positive light shed on this inflation release, we see some complacency. Inflation is still nearly twice the Bank of England target and supply seems a much more important, and uncontrollable, factor than demand in the equation.

In the US, Trump tariffs, albeit far from certain, have injected the possibility of higher inflation. At best this could be a one-off adjustment to the price level, which is either passed on quickly or absorbed in corporate margins, before being passed on later. Recent reports suggest we’re seeing more of the latter. This may not make a significant difference to inflation expectations. However, it has been coupled with talk of tariff windfall payments, which raises the prospect of introducing a dangerous feedback loop.

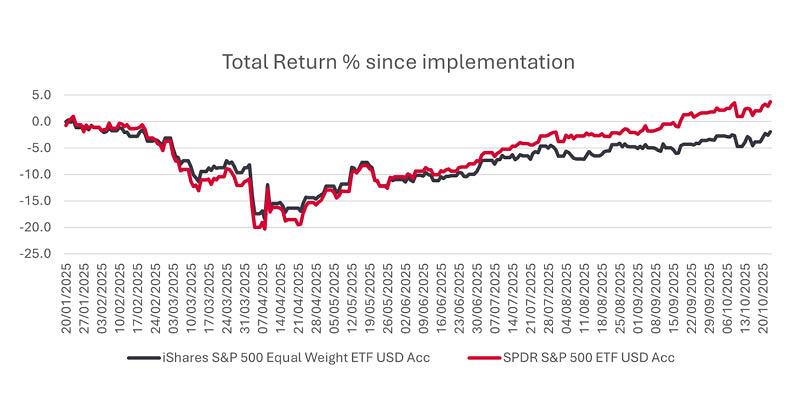

Moving back to equities, concentration has worsened within equity markets. Nvidia in the US is now a larger component of the global equity market than the UK, Japan and China individually, and Germany and France combined.

To ensure that the US equity allocation with the AJ Bell funds and Passive MPS behaved as expected in terms of volatility, we introduced the iShares S&P 500 Equal Weight ETF in January.

There have been signs that we are right to try navigating concentration risk, but so far it has been a performance detractor – as shown in the chart.

Source: Morningstar Direct, Total Return in GBP from 20/01/2025 to 23/10/2025. No rebalancing impact is assumed and therefore this does not represent actual portfolio level performance.

The position was sized conservatively, at around 15% of US equity exposure, and we continue to assess it. As the market increasingly herds into the AI theme, we are also on the lookout for opportunities that have been left behind.

As we look ahead to the crest of 2025, and to the hills beyond, we see reason to be active asset allocators, but sparingly so. Too many TAA decisions pose a risk of derailing the SAA, and we shouldn’t be distracted from the path we’re following. The benefits of SAA diversification have been on show this year as the wider opportunity in global equity markets has come to the fore. When it comes to TAA, a large part of our time is spent assessing that inbuilt diversification of the SAA, to make sure it’s working as it should.

If you’d like to take a closer look at the path ahead, please get in touch. Our solutions are well placed to support your clients’ goals as we move from 2025 into new territory.

The value of investments can go down as well as up and your client may not get back their original investment.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.