Pension tax rules are forever changing. In the last 25 years there have been changes almost every April.

But even against this background of constant change, April 2015 stands out like a beacon, launching the double whammy of the landmark pension freedoms giving more flexibility on accessing pension savings, and the new generous tax rules on death.

The world before pension freedoms now seems strange. Then, most people (75%) used their pension fund to buy an annuity, and policy makers were wrestling with the challenge that most people stayed with their current provider instead of shopping around for better rates.

Drawdown was the preserve of the few. The rules setting the maximum amount of income from capped drawdown were inflexible. The alternative – flexible drawdown – gave you more freedom, but you had to have a guaranteed income of at least £20,000 a year (falling to £12,000 in March 2014).

The former Chancellor George Osborne’s words “no-one will have to buy an annuity” were a breath of fresh air. Overnight the world changed, and people could take as much money as they wanted from their pension savings to match their needs in retirement.

So, what did people do with their new-found freedom?

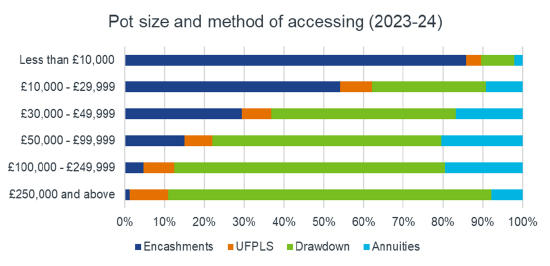

If we look back, the world has flipped upside down. Over the last ten years, around 10% of AJ Bell’s estimate of seven million people who have accessed their pensions bought annuities, as they quickly fell out of fashion. And although this proportion might have nudged up in the last year, given current rates, it is unlikely to reach its previous highs.

Instead, drawdown is by far the most popular option for people accessing pots of £30,000 or more, used by 60% last year. A further 8% used uncrystallised funds pension lump sum (UFPLS) payments, the new form of taxable lump sum payments launched alongside flexi-access drawdown in 2015. Last year, among those with £100,000 or more in their pension pot, the vast majority opted for flexibility through either drawdown (73%) or UFPLS (9%), while just 15% bought an annuity.

The most popular option in 2023-24 was to take an income withdrawal rate of 8% or over. While there may be valid reasons for taking income at above 8% – for example, people taking their income solely from one pension whilst leaving others untouched – others might need more support to understand the consequences of their actions.

However, an 8% withdrawal rate was more popular for smaller drawdown pots, with the average withdrawal rate falling to more moderate levels from larger pension pots. Among those with £100,000 or more in their pension pot, 65% withdrew less than 6% income last year, with 44% taking under 4%.

Perhaps one of the biggest headlines from pension freedoms was the ability to fully encash the pension pot. Certainly, there were some concerns as we edged ever closer to 6 April 2015 that people would simply blow the lot. Many headlines covered the remark by Steve Webb, the then pensions minister, about people buying Lamborghinis.

However, these fears were unfounded. Around 55% of pension pots have been fully encashed since 2015. However, when you delve into the numbers the vast majority (90%) were small pots worth less than £30,000.

Pension freedoms have greatly benefited millions over the past decade, helping them to use their pension pot in the best way for them. Financial advisers and planners have been there with them every step of the way, making sure their clients use their flexibility to secure the income they and their family need in their later years.

Source: FCA Retirement Income Market Data

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.