After a close run defeat in the previous year, the rematch was set for May 1997 in the heart of New York. However, unlike other heavyweight tussles, this was not battle in the ring, but rather across a chess board.

In what was dubbed at the time as ‘Man vs Machine’ the defeat of World Chess grandmaster Garry Kasparov by IBM’s supercomputer Deep Blue was heralded as the vanguard of Artificial Intelligence (AI).

This defeat was the culmination of over 30 years of computing effort to develop software that could beat the best human chess players on the planet - yet it was seen by many at the time as merely a vanity project of the computer geeks; the endgame was a computer that could beat a grandmaster at chess, and had no other practical use. However, to quote the great man himself, “…while the era of human versus intelligent machine was ending in chess, it was only getting started in every other aspect of our lives.”

Fast forward twenty years to 2017, and this time it was Google’s DeepMind Project that led to the defeat of the grandmaster of an even more complex game, the ancient Chinese strategy game, Go. Despite the advances in computing power, a computer still did not have the processing power to beat an expert at the game by memorising all the possible moves and playing the ‘most valuable’ move each time; with 10360 (that’s a 10 followed by 360 zero’s!), possible sequences of moves for any given game. Based on the average computing power of a standard processor (109 operations per second), it would take longer than the age of our universe to evaluate all the possible moves.

10,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000 |

Instead, AlphaGo Zero learns to play from scratch. It follows the process of a human brain, playing games over and over again, learning from its mistakes, refining and improving the rules it follows. Once it has done this it repeats the process from scratch, but instead of playing itself, it plays against the previous version of itself. Remarkably, this means no human input is needed in the learning process, and AlphaGo possesses strategies not known to humans!

This process of building what is known as a neural network has applications beyond that of an ancient Chinese strategy game. DeepMind has already found many new uses for its technology, such as reducing the amount of energy needed for cooling data centres by 40%, or improving the recommendations made by smart assistants such as Siri, Alexa or Google Assistant. Google recently announced its new Google Duplex technology, which enables seamless conversations between humans and machines, helping to improve productivity, and as such helping drive economic growth.

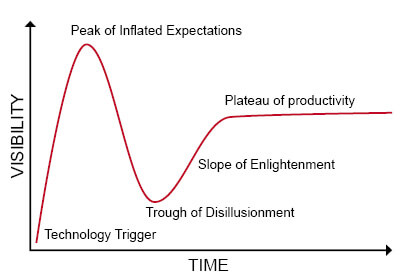

Any new technology tends to go through the same life cycle. The idea emerges, with investors getting excited and reaching a level of inflated expectations. As the complications of implementing the idea arise, such as data protection or commercial viability, disillusionment often follows. However, these are often ironed out before the idea comes into fruition and turns a profit.

We believe after 20 years in the pipeline AI is finally reaching a stage where investments in profitable companies can be made. As an example, both robotics and automation benefit from the use of AI, and are both widely investible themes. They are no longer niche industries confined to the technology sector – John Deere, the tractor maker, recently spent $305m on purchasing the technology for an automated weeding robot!

Source: Gartner

With major asset classes such as UK, US and European equities now highly correlated, portfolios can benefit from the extra diversification achieved by investing in sectors that offer different sources of risk. Any investment in cutting edge ideas carries high standalone risk, but as part of a portfolio can help enhance the returns for the given level of risks. In the last decade the technology sector has doubled its weighting in the MSCI World Index, whereas sectors such as Energy have nearly halved. When investing for retirement it is important to focus on a long-term horizon, and what the future makeup of the markets will be. We believe the world’s economy will become increasingly reliant on the technology sector to deliver economic growth and will be a predominant factor driving the return of global equities over the next decade.

As ever the financial industry has reacted to investor demand, with both active and passive fund managers launching thematic products exposed to new technologies such as robotics, automation, cyber security and digitalisation. However, when making an investment in any of these sectors it is important to understand how the investment process identifies companies that will benefit from the trends – it is important to not just invest in companies such as DeepMind, but to also make sure the product contains investments in the users of the technology, such as John Deere.

A portion of AJ Bell’s new Global Growth fund invests thematically; our approach is to look for investment products that consider the entire supply chain of the emerging technology. Incidentally, we believe this can be achieved passively through the use of AI and big data. Index providers are able to use the data they have on a large universe of public companies to identify, through a set of dynamic rules, which corporations are part of the supply chain, not just the big companies that have already benefitted from the theme.

By investing in a diversified basket of shares the fund moves the risk of a large loss driven by individual companies or technologies failing (think Betamax vs VHS!), whilst giving us exposure to areas which we feel will be a larger part of the financial markets in the future.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.