A bout of market volatility meant the traditional summer lull didn’t last for long this year. Fears over global growth became more widespread as the quarter wore on, whilst concerns over inflation moved out of the foreground. Meanwhile, the certainty provided by the UK election and the resilience of economic data brought UK markets into favour. The pound appreciated and so caused a headwind for overseas investments.

The US economic outlook has become more uncertain in the eyes of many. While some elements of the economy are steady, employment data started to soften. Investors now seem to have a heightened awareness of downward revisions to the historic data that has hitherto cast the US as a beacon of economic stability.

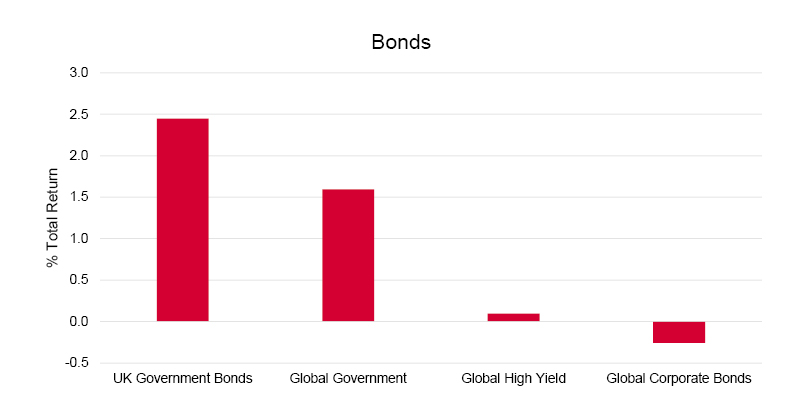

Coupled with further signs of moderating inflation, albeit still above target, the sustainability of current interest rates came back into focus. The Fed subsequently initiated their cutting cycle with a slightly more aggressive than usual 50bp lowing of rates. This drove a steady rally in US Treasury yields and a weaker US dollar over the summer.

Other global government bond yields tentatively followed. Credit spreads joined some of the equity market volatility, however remained at relatively tight levels historically speaking.

Source: AJ Bell, 01/07/24 to 30/09/24. Total returns represent those in GBP terms.

Signs of volatility emerged in July as AI related stocks began to swing wildly. Although the US was naturally the centre of attention given the sheer scale of some of the stocks, it was in fact Japan that became the epicentre of the August volatility that reverberated around markets.

A slightly more hawkish tone from the Bank of Japan when raising interest rates to 0.25% sent the yen on a sharp rally. Given the yen has been a funding currency for markets for several years, this sent a shockwave of deleveraging across several asset classes. The tentacles of a so called ‘carry trade’ are not easily identified, however it serves as a reminder of how volatile and short-term-focused markets can be. By quarter end the impact of the volatility was scarcely visible, with most markets recovering quickly and the issue drifting from focus.

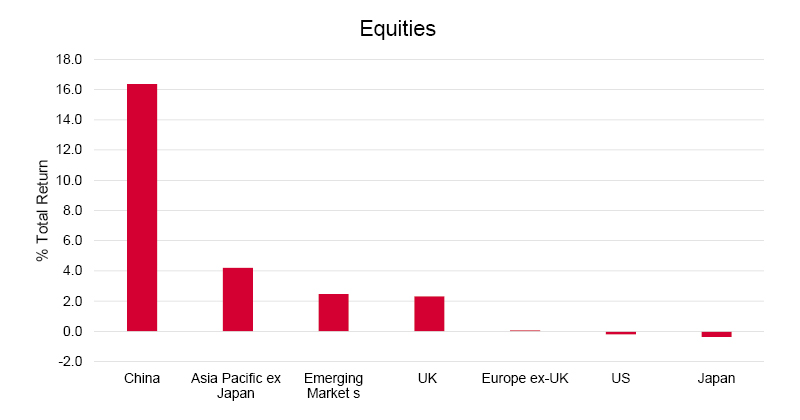

Closer to home, the UK equity market emerged as a strong performer. The more domestically orientated mid and small cap indices performed particularly well owing to the combination of clearing of political uncertainty and relatively good economic data.

Elsewhere, the Chinese government surprised markets in the last week of the quarter with a volley of stimulus announcements. This prompted a significant rally in Chinese equities, akin to the rebound from the Global Financial Crisis, and in turn moved Asia and Emerging Market indices from being some of the worst performing globally in the quarter, to the best, in the space of just one week.

Source: AJ Bell, 01/07/24 to 30/09/24. Total returns represent those in GBP terms.

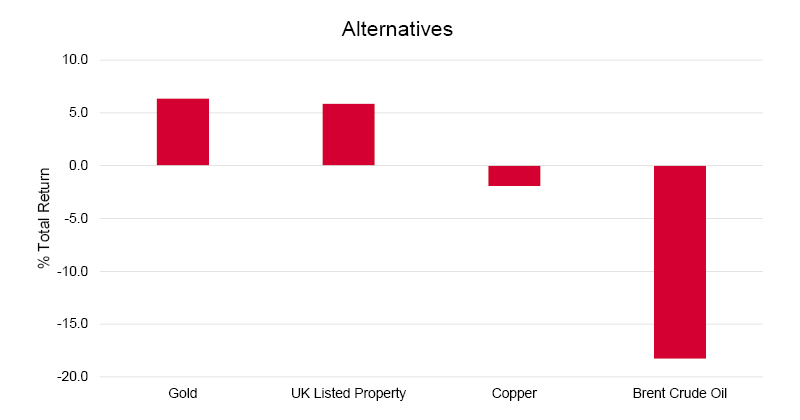

UK Property also performed well during the quarter, consistent with a return to favour in more pro-cyclical areas of the UK market such as mid and small caps. Gold continued to rally with investors now more focused on interest rate cuts and therefore the relative incentive to own an asset with no yield. Wider commodity prices, such as oil and industrial metals, broadly declined over the quarter on concerns over economic growth, particularly in China.

Source: AJ Bell, 01/07/24 to 30/09/24. Total returns, where applicable, represent those in GBP terms.

As we mentioned last quarter, the state of economic growth is likely to continue. China is still grappling with issues in the property sector, but there are now signs the authorities may be willing to grasp the nettle and in doing so set the economy on a new more technologically-aligned growth path. Clarity on messaging from the various Chinese government departments may prove to be key here and is not a given.

Elsewhere, politics will return to the fore with the November US election. Aside from that, markets will be interested in the messaging from the Fed around any further cuts to interest rates for signs of short-term concern.

Our focus, as ever, will be on the long term and keeping a lookout for opportunities.

The Investment Asset is a hub for all the priceless information and content generated by our Investment Team. Bringing together news on the latest market trends, investment analysis and performance reports for our AJ Bell Funds and MPS ranges, it’s the perfect way to keep up to date on the opportunities that exist for your clients.

The value of investments can go down as well as up and your client may not get back their original investment.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.