Vehicles investing in warehouses and self-storage have done pretty well despite the gloomy headlines.

If you’d been keeping an eye on news from the UK commercial property market, you might be forgiven for thinking the sector was a complete basket case.

Bankrupt retailers have left gaping holes on the high street, while office occupancy has been decimated by the pandemic.

Meanwhile many open-ended commercial property funds suspended trading for over a year, with some ultimately shutting their doors permanently. There has undoubtedly been a great deal of upheaval in the commercial property market, and risks remain, but it certainly hasn’t been a tale of woe across the board.

Like many other parts of the economy, commercial property has been deeply influenced by global trends that we are perhaps more accustomed to thinking about through the lens of the stock market. Technological changes have led to a more digitally enabled consumer, and in the commercial property space, that has meant hot demand for the logistical hubs that facilitate the UK’s online delivery services.

The flip side of that coin is that traditional retail outlets have been hammered by the shift from bricks to clicks, which was of course exacerbated by the pandemic. Clearly there is also considerable uncertainty over the future of office space, as businesses shift to flexible working practices.

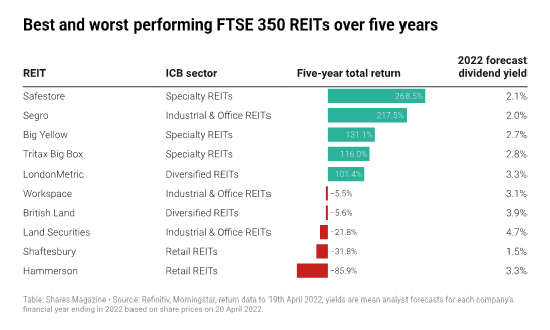

It’s no surprise, then, to see some pretty polarised performance from REITs (real estate investment trusts), which invest in commercial property. The REITs that performed best in the last five years have been those with minimal exposure to office space and retail. Both Safestore (SAFE) and Big Yellow (BYG) have performed well, offering secure self-storage facilities to individuals and businesses, no doubt helped along by small online businesses looking for somewhere accessible to stash their stock.

Meanwhile Segro (SGRO) and Tritax Big Box (BBOX) have also prospered, by providing industrial warehouse units that serve to fulfil online orders.

Things look considerably different at the other end of the performance table. British Land (BLND) and Land Securities (LAND), two major players in London office and retail space, have both posted extremely disappointing returns. But it’s the REITs with higher levels of retail exposure, Shaftesbury (SHB) and Hammerson (HMSO), which sit at the bottom of the pile. The pandemic was simply devastating for the shops, restaurants and cafes these trusts hold in their portfolio.

Clearly a lot of expectation is now baked into the valuations of the victors, and a lot of pain is already in the price of the losers. This is reflected in the lower yields investors typically have to accept to invest in the areas that have structural tailwinds behind them.

Like in the stock market, investors are faced with paying up for growth, or seeking out value opportunities. In order to avoid getting caught short by either an elongation, or a reversal, of market trends, it therefore makes sense to maintain some balance in a commercial property portfolio, rather than going for broke on growth or value.

However, the disruptive rise of e-commerce is not the only risk commercial property investors need to consider. The asset class is popular for the income it provides, and that appeal may wane somewhat as interest rates rise. In a world starved of yield for more than a decade by loose monetary policy, anything that provides income has proved attractive to investors. This does pose a threat to flows into the commercial property sector, because investors might start looking at bonds more favourably, as yields are pushed up by central banks raising interest rates to deal with inflation.

However, it seems unlikely that any flood of money out of income-producing assets like commercial property and into bonds would take place when interest rates look like they are still rising. Why buy a bond paying 2% interest today when you could buy one paying 3% tomorrow?

And as long as inflation is looking problematic, investors will also probably show a preference for real assets like commercial property, which can provide at least some protection from rising prices. Commercial property can do this through explicit annual uplifts in rental agreements, or through regular rent reviews for shorter leases.

While commercial property does offer some protection from inflation, the wider economic picture is also a risk to consider, because investors ultimately rely on businesses to occupy premises, and pay rent. A more constrained consumer would dent their ability to do that, and wherever you look, economic forecasts for the UK next year are not looking pretty. Of course, the crystal ball gazers don’t have an unerringly accurate view of the future, and plenty of investors will still look to commercial property to provide an income, and work as some diversification in a portfolio.

Investors have a choice of using closed-ended investment trusts, or open-ended funds to gain exposure to commercial property. Investment trusts are more volatile, but they do offer instant liquidity, though that may come at a price in times of market stress. By contrast, open-ended funds imposed lengthy trading suspensions after Brexit, and during the pandemic.

To try to forestall this, open-ended funds now hold cash balances as high as 20% of the portfolio to meet any investor withdrawals, which is a lot of money to be sat there not doing very much.

On balance, those who want to gain exposure to commercial property are probably best off doing so through investment trusts, and diversifying across industrial, office and retail opportunities.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.