Emma is aged 54 and is keen to maximise her pension savings as she plans for her retirement in a few years’ time.

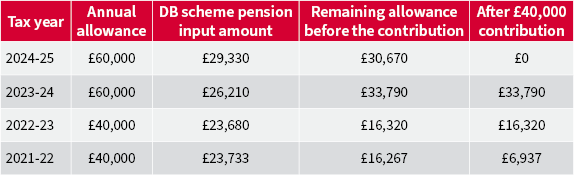

She is a director of a small company. At the end of last tax year, the company paid in a pension contribution from their limited company to her for £40,000, relying on using carry forward. She also has a defined benefit work pension scheme, and the pension input amount was just over £29,000 last year.

Emma earns about £120,000 from her employment. She also has a separate self-employed role, from which she earns around £50,000. She wants to make additional pension contributions and wants to know how much she can make.

Working out how much Emma can pay depends on the accumulated value of her earnings and of her pension contributions.

First, Joe – Emma’s financial adviser – works out how much unused annual allowance the £40,000 contribution used up, and how much unused annual allowance she has left.

Joe then considers what could happen this tax year. To do this he has to make several assumptions about what the 2025 pension input amount (and therefore Emma’s employed salary as well as future rates of CPI) and what her self-employed income will be.

Obviously, this is difficult, so he may just want to use the same amount as the previous years.

If he assumes her pension input amount will again be £29,000 then her unused annual allowance for 2025-26 will be £31,000. If he adds this to her unused annual allowance from the previous three tax years, this gives a total of £81,110 (the tax year 2021-22 ‘drops off’ the calculation).

This means Emma could pay an additional £81,110 into her pension using her savings. This is below the combined value of her employed and self-employed earnings, meaning she should get full tax relief on the contribution.

If she makes a £64,888 net contribution into her SIPP, then together with the basic rate tax relief added by HMRC this would bring the total to £81,110. As she’s a higher rate taxpayer she can then make a claim with HMRC for her remaining tax relief, either through her self-assessment or by completing a claim online.

The upside of making a pension contribution at the start of the year is it has the potential for another full year of tax-efficient investment. But the downside is that Emma and Joe have to make several assumptions regarding future events, which may not come true.

The best route forwards is probably for Emma to make a lower pension contribution now – say £70,000 – and then to top up towards the end of the tax year when she will have a better sense of how much unused annual allowance she has left.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.