The UK needs to act to close the savings gap and ISAs are the perfect product to help people build their financial resilience and prosper in the future. But they are currently too complicated – savers are faced with too much choice. Instead, they need a simple solution to help kickstart their savings.

Although ISAs have become a recognisable and trusted savings vehicle, complexity and lack of understanding remains one of the biggest barriers to investing. Only half the people in our research could correctly identify the main types of investment ISA and less than a third know the annual ISA allowance is £20,000*.

A One ISA system would help to encourage competition, making it easier for customers to compare just a single type of ISA product and switch between different providers. It would also eradicate much of the tax and product complexity that could eventually see ISAs turned into a political football in the same way as pensions taxation.

There are currently six different versions of ISAs in the UK, each with different aims and some with different allowances.

Simplifying ISAs by creating a single ‘One ISA’ encompassing both savings and investments would reduce complexity, boost competition and remove the need for ISA customers to choose between the multitude of different account types available today.

Switching would become far easier, with customers able to hold cash, investments, or both in their account, and move between providers freely, whereas today’s ISA market is divided down the middle between investing and cash savings accounts.

It would also end the proliferation of ISA products, which risks endangering their success by creating overwhelming choice and opening the door to undue complexity with different rules, restrictions and terms of withdrawal for each product.

The FCA has recognised there are around 8.6 million people holding more than £10,000 of investible assets in cash and wants to encourage more people to think about investing. A simplified ISA system would make it far easier for cash ISA savers to start investing some of their money, without the need to open up an entirely new stocks and shares account.

The removal of the LTA is a gamechanger for pension savers and finally ends the unfair punishment of pension savers who have diligently set money aside for later life and been rewarded with strong investment growth.

However, legislation to support this complex transition remains incomplete, with little time remaining for it to be finalised and implemented ahead of the new tax year. It’s still not clear how HMRC intends to tax drawdown income where the member dies before age 75 and there is a real danger of unintended consequences and serious confusion for savers.

To reduce confusion and ease the transition for pension savers, the new legislation needs to be simple, avoiding unnecessary complexity. But the compressed timescale remains a serious challenge, and a later implementation date of April 2025 is more achievable.

Efforts by the government and the FCA to improve the help available to savers and investors through the advice guidance boundary review are extremely welcome.

However, in our view there is little demand for simplified advice among the adviser community. Advisers offer an incredibly valuable service to their clients, but the economic reality of providing professional financial advice means it isn’t practical for the mass market.

While some providers – likely large institutions – may be able to offer simplified advice at scale, this risks shoe-horning consumers into taking advice at additional cost, when in fact many simply require a little help to understand their options.

Instead, efforts should be trained on allowing providers without advice permissions to provide customers with additional practical help and support that doesn’t constitute advice.

It will likely take a step-change in the approach from the regulator to shift attitudes towards this, since providers currently err on the side of caution and avoid anything that could be misconstrued as financial advice. The Consumer Duty provides an ideal platform to initiate that step-change and creating a simpler, more defined guidance regime that could give firms the necessary confidence to deliver more useful, personal communications with the aim of achieving good outcomes for consumers

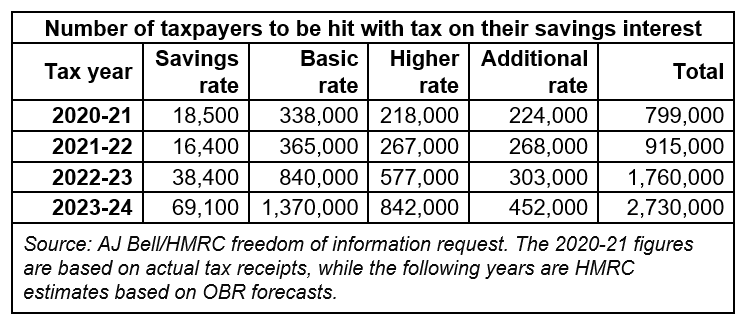

We continue to call on the Chancellor to end the freeze on the personal savings allowance, which has been set at the same level since 2016.

The number of people set to pay tax on cash savings interest is set to rise by a million this year alone (see table), as a consequence of the frozen threshold which has not been adjusted to reflect inflation and rising interest rates. This includes over 1.4 million basic rate taxpayers and low earners, demonstrating that this tax is impacting everyday Brits, as well as wealthy individuals with large sums in cash.

Individuals pay tax on interest they earn on cash savings that exceeds the Personal Savings Allowance, which currently stands at £1,000 for basic rate taxpayers and £500 for higher rate taxpayers. Additional rate taxpayers get no exemption and pay tax on all cash interest they receive.

Tax bills are paid either through self-assessment, or deducted from income through a tax code adjustment. Many won’t be aware that they owe the tax until HMRC sends them a letter to change their tax code to deduct the money from their payslip. It shouldn’t be the case that ordinary savers are caught up in tax complexity for doing the responsible thing and building a savings pot.

Doubling the personal savings allowance would mean that £20,000 held in a 5% savings account would not be taxed for basic and higher rate taxpayers, ending the penalty on those who do the responsible thing by building up a cash savings buffer for a rainy day.

During the pandemic the government reduced the withdrawal charge on Lifetime ISAs from 25% down to 20%, to allow people to access their savings penalty-free if they found their finances squeezed during the crisis. Disappointingly, this was restored to 25%, rather than changed permanently.

It feels impossible that the government doesn’t view the current cost-of-living crisis in the same way. Reducing the exit fee would be a low-cost move for the government that would help first-time buyers who saved into their Lifetime ISA in good faith but, due to soaring inflation, now need to dip into their savings.

Data collected by AJ Bell via Opinium. Survey of 2,000 UK adults conducted March 2023

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.