Among a raft of changes, Chancellor Rachel Reeves announced reform to salary sacrifice as well as increases to tax on property, savings and dividend income as she attempts to bridge the gap between spending and revenue in the UK’s finances.

The protracted leadup to the Budget included rumours around gifting limits and a hike in income tax. However, these were not introduced. Instead, tax rises are centred on dividends, savings income, and additional council tax for high-value properties. Tax threshold freezes will also continue for three years, and the rules around salary sacrifice will change so that pension contributions over £2,000 will be subject to National Insurance.

The subscription allowance of cash ISAs will be reduced to £12,000 each year for those under age 65. Stocks & shares ISAs remain at the £20,000 limit.

Here’s a breakdown of the main policy changes in the Budget, when they come into play, and how they could affect your clients’ finances:

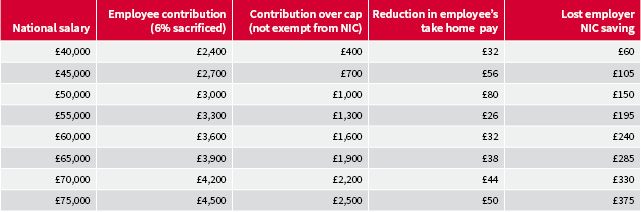

From April 2029, there will be a £2,000 limit on National Insurance savings on salary sacrifice pension contributions. Anything above this amount will be subject to both employee and employer National Insurance contributions.

Salary sacrifice currently helps workers save up to 8% in employee National Insurance on the cost of their pension contributions, in addition to income tax relief. Employers also save their 15% National Insurance contributions.

The below table shows the impact on employees’ pay packets a year, assuming the employee has agreed to exchange 6% of their notional salary for a pension contribution, with a 6% employer match (and that the employer does not share any of their National Insurance savings).

The impact of a salary sacrifice limit

Source: AJ Bell. Figures based on when the changes happen in 2029.

Despite the new salary sacrifice savings limit, personal pension contributions will still be exempt from income tax and workers can continue to enjoy pension tax relief at the current levels. Plus, making pension contributions will still reduce a taxpayer’s ‘adjusted net income’, pulling them out of higher rate tax while also boosting their retirement savings.

Employers have been given a relatively long lead-in time of over three years to work out how to re-position their employees’ pension savings. Some will consider scrapping the salary sacrifice arrangement and instead ask employees to pay pension contributions from their salary. Others will keep the salary sacrifice arrangement in place to benefit the first £2,000 pension contribution. Anyone earning £40,000 or less where their pension contribution is 5% a year should not be affected.

Whatever route employers take they face the loss of their National Insurance contribution saving. Some may choose to reduce future wage growth and instead provide employees with higher employer pension contributions – although this arrangement would potentially have to be agreed with the entire workforce to avoid clashing with employment law.

The Government has announced it intends to scrap the lifetime ISA and replace it with a new simpler ISA product to support first-time buyers to buy a home. It will consult on this new ISA in early 2026.

However, lifetime ISAs are also used by the self-employed – and others – as a way of saving for retirement. The Pensions Commission is only just up and running, and will be concentrating on improving the outcomes for those on lowest incomes, as well as the self-employed. It therefore makes sense that no big decisions are taken on the future of the lifetime ISA until the Pensions Commission concludes its work.

While stocks & shares ISAs will maintain their £20,000 annual subscription allowance, cash ISAs will have a £12,000 limit each year beginning in April 2027. This limit will not apply to those over the age of 65.

We do not yet know if this change will be accompanied by a restriction on transfers from stocks & shares ISAs to cash ISAs, or any other complexity.

Income tax threshold freezes have been extended for another three years until April 2031, meaning income bands will be on track to stay the same for a decade. The nil rate band threshold for inheritance tax (IHT) has also been extended to April 2031.

The extension of the income tax thresholds will drag more clients into paying higher rates of marginal income tax. Clients may want to explore options to reduce their income tax liability such as topping up pension contributions, using salary sacrifice if possible, making gifts to charity, or reshaping remuneration, for example business owners taking more in dividends.

Both basic and higher rate taxpayers will face an increase of two percentage points in the amount they pay on dividend income starting in April 2026. This means that basic rate taxpayers will now face a 10.75% tax while higher rate taxpayers face a 35.75% tax. There is no tax increase for additional rate taxpayers from their current 39.35% rate.

Clients may want to consider moving their investments to within a tax wrapper such as a pension or an ISA before April 2026 to reduce the tax paid after that date. Outside these wrappers, clients still have a £500 tax-free dividend allowance before they begin to be taxed at the above rates.

Savings income will also see a 2% tax increase for all levels of taxpayer beginning in April 2027. Basic rate taxpayers will then pay 22%, while those in the higher and additional rate brackets will pay 42% and 47% respectively.

Starting from April 2027, new separate tax rates for property income will be introduced. The basic property rate will be 22%, the higher property rate will be 42% and the additional property rate will increase to 47%.

Starting in April 2028, owners of properties valued at over £2,000,000 will be subject to an additional yearly tax – a ‘mansion tax’ – collected at the same time as council tax, although the revenue will flow to central government rather than remain with local government.

This surcharge will begin at £2,500 a year and scale in bands to £7,500 a year for properties valued at £5,000,000 or more. These will increase in line with consumer price inflation (CPI) each year.

The value of the property will not be determined using current council tax methodology.

The OBR predicts this tax will be factored into the price of properties over time and create price bunches below each band on the scale. There will be a deferral scheme for those unable to pay immediately, and the Government will consult on the details.

Unused pensions will be brought into the calculation of IHT from April 2027, as previously proposed. Under the proposals personal representatives (PRs) are responsible for calculating and paying the IHT due from the pension scheme.

There will be a tweak to the proposed process to give the PRs the power to ask the pension scheme to withhold 50% of the taxable benefits for up to 15 months and to pay the IHT due in certain circumstances. The PRs will also no longer be liable for the payment of any IHT due on pensions discovered after they have received clearance from HMRC.

This will give PRs some much needed flexibility to pay the IHT due. However, a better solution would have been to find a completely different way of taxing pension benefits on death – something most of the pension industry have spent the last year urging HMRC to do. It’s disappointing that HMRC has chosen again to stick with the hard administrative path, rather than thinking about the grieving families who will sadly get caught up in this administration nightmare at the time they are most vulnerable.

There will be further changes to the policies for new rules announced last year. The £1 million allowance for the 100% rate of agricultural property relief and business property relief will be transferable between spouses and civil partners. The Government will also make changes to the way internationally mobile individuals are taxed, closing loopholes and capping relevant property trust charges payable by certain trusts.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.